Losing a job is stressful on its own, but for many people, the bigger surprise comes when they see the COBRA health insurance cost for the first time. What once felt affordable through an employer can suddenly become one of the largest monthly expenses in a household budget.

COBRA health insurance is designed to help people keep their existing coverage after a job loss or reduction in work hours. While this sounds reassuring, many individuals quickly discover that the COBRA insurance cost is much higher than they expected. This happens because the employer is no longer paying part of the premium, leaving the full amount up to the individual.

If you’re wondering how much COBRA insurance costs, why it feels so expensive, and whether there are more manageable options, you’re not alone. This guide will break down the real costs, explain why prices are high, and help you understand what you can do next.

Compare affordable health insurance options today!

What COBRA Actually Is

COBRA is a federal law that allows you to temporarily keep your employer-sponsored health coverage after certain life events that would normally cause you to lose it. The name comes from the Consolidated Omnibus Budget Reconciliation Act, and it applies to most employers with 20 or more employees who offer group health insurance.

Instead of enrolling in a brand-new plan right away, COBRA lets you stay on the same health plan you had while working. That means you usually keep the same doctors, hospital network, and covered services. For many people, this continuity can feel reassuring during a time of change.

COBRA is commonly offered after events like job loss (not due to serious misconduct), reduced work hours, divorce, or when a dependent child no longer qualifies under a parent’s plan. Coverage typically lasts up to 18 months, though in some situations it can extend longer.

Understanding what COBRA is helps explain why the COBRA health insurance cost can be high. You are keeping a full employer plan, but the way it’s paid for changes.

How Long Do You Have to Decide on COBRA?

After losing job-based coverage, you do not have to decide immediately, but there is a deadline. You generally have 60 days from the date you receive your COBRA election notice, or from the date your coverage would otherwise end, whichever is later, to choose COBRA coverage.

If you elect COBRA on day 59, your coverage is retroactive to the day your employer plan ended. This means you will still owe premiums for that earlier period. Understanding this timeline is important when comparing the COBRA health insurance cost with other coverage options, since delaying a decision can lead to a large first payment.

How Much Does COBRA Health Insurance Cost?

One of the first questions people ask after losing job-based coverage is, how much does COBRA insurance cost? The answer can be surprising. The COBRA health insurance cost is usually much higher than what you paid as an employee because you are now responsible for the entire premium.

On average, the COBRA insurance cost can range from $400 to $700 per month for an individual and $1,000 to $1,800 or more for a family. These numbers vary depending on your employer’s original plan, the number of people covered, your location, and the insurance company behind the policy.

When you were employed, your company likely paid a significant portion of the premium. Under COBRA, you pay both your share and the employer’s share, plus up to a 2% administrative fee. That small extra fee may not sound like much, but combined with the full premium, it makes a noticeable difference. See average health insurance costs and what impacts pricing

This is why many people who search “COBRA health insurance cost” or “is COBRA insurance expensive” are caught off guard. The coverage itself hasn’t changed but the amount you pay each month has.

Why COBRA Costs So Much

After seeing the numbers, many people wonder why the COBRA health insurance cost is so high compared to what they paid while working. The main reason is that the structure of payment changes completely, even though the plan itself stays the same.

Loss of Employer Contribution

When you were employed, your employer likely covered a large portion of your premium, sometimes 50% to 80% of the total cost. Once you switch to COBRA, that financial support disappears. You take on the entire bill, which is why the COBRA insurance cost suddenly feels overwhelming.

Keeping a Comprehensive Group Plan

Employer-sponsored plans are often broad and include large provider networks, lower copays, and strong prescription benefits. These features make the plan valuable, but they also make it expensive. Under COBRA, you’re still enrolled in that same comprehensive plan just without the employer’s help paying for it.

No Income-Based Savings

Unlike plans purchased through the ACA marketplace, COBRA does not offer financial assistance based on income. Whether you earn a little or a lot after leaving your job, the COBRA health insurance cost stays the same. This lack of flexibility is a major reason people start looking for alternatives.

Administrative Fees

COBRA coverage can include up to a 2% administrative fee. While small compared to the full premium, it still adds to the total monthly amount you must pay.

Together, these factors explain why so many people search “why is COBRA insurance so expensive” after leaving a job. The coverage hasn’t become more expensive; you’re simply seeing the true total cost for the first time.

Situations Where COBRA May Still Be Worth the Cost

Even though the COBRA health insurance cost is high, there are situations where keeping COBRA coverage can make financial or medical sense.

- You’ve already met your deductible

If you’ve paid a large portion of your yearly deductible, switching plans could mean starting over. Staying on COBRA may help you avoid paying those costs again. - You’re in the middle of treatment

Ongoing surgeries, cancer treatments, or specialist care may be easier to continue under your current plan rather than switching networks. - Your doctors may not be in other networks

Some provider networks differ between plans. COBRA lets you keep the same doctors and hospitals without disruption. - You only need short-term coverage

If you expect to start a new job with benefits soon, paying the COBRA insurance cost for a few months may be simpler than changing plans twice. - Your prescriptions are well-covered under your current plan

Drug formulas vary. Staying on COBRA can prevent unexpected medication cost changes.

In these situations, the higher COBRA health insurance cost might be balanced by stability and continuity of care.

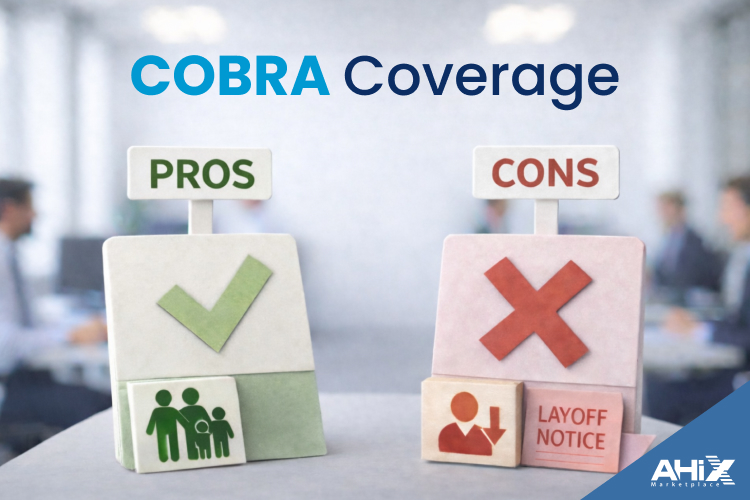

COBRA Pros and Cons at a Glance

Before deciding, it can help to look at the advantages and disadvantages side by side.

| Pros of COBRA | Cons of COBRA |

| Keep the same doctors and hospital network | Very high monthly premium |

| No need to change health plans right away | No income-based financial assistance |

| Helpful if you are mid-treatment | Total costs can add up quickly |

| May avoid restarting your deductible | Limited flexibility in plan choices |

This overview helps explain why the COBRA health insurance cost may be worth it for short-term stability, but difficult to manage over a longer period.

When COBRA May Be Too Expensive to Sustain

For many households, the COBRA health insurance cost simply doesn’t fit into the budget long term. While the coverage is solid, the monthly premium can create financial pressure, especially after a loss of income.

Here are situations where COBRA may feel unaffordable:

- Your monthly premium takes a large share of your income

If a significant portion of your paycheck would go toward the COBRA insurance cost, it may not be sustainable for many months. - You’re generally healthy and don’t use much medical care

Paying for a high-cost, comprehensive plan may not make sense if your healthcare needs are minimal. - You expect to be between jobs for a while

COBRA might work short-term, but over 6-18 months, the total cost can add up to thousands of dollars. - You qualify for income-based savings elsewhere

Marketplace plans may offer premium tax credits that lower your monthly cost, which COBRA does not provide. Learn how health insurance marketplaces work! - Your financial priorities have changed

After job loss, expenses like rent, mortgage, and daily living costs may take priority over a very high insurance premium.

If you’ve been asking “is COBRA insurance expensive?”, you’re not alone. For many people, the cobra health insurance cost becomes a signal to start comparing other coverage options that may better match their new financial situation.

What You Can Do If COBRA Is Too Expensive

If the COBRA health insurance cost feels out of reach, you still have other ways to get coverage. Losing job-based insurance qualifies you for special enrollment opportunities, and comparing alternatives could help lower your monthly premium.

Here are options to consider:

- ACA Marketplace Plans

Losing employer coverage opens a Special Enrollment Period, so you don’t have to wait for the annual Open Enrollment. Many people qualify for income-based premium tax credits, which can make marketplace plans significantly cheaper than the typical COBRA insurance cost. This is often why people compare COBRA vs marketplace insurance when searching for better rates. - Check If You Qualify for Medicaid

If your income dropped after job loss, you or your family members may qualify for Medicaid. In many states, this means low or even zero monthly premiums. - Join a Spouse or Partner’s Employer Plan

A loss of coverage can allow you to enroll in a spouse’s or partner’s workplace plan outside their usual enrollment period. - Consider Short-Term Health Insurance

These plans often have lower premiums than COBRA, but they usually provide more limited coverage. They may be an option if you need temporary protection and are generally healthy. - Compare Plans Side by Side

When you’re evaluating alternatives to COBRA insurance, it helps to look at premiums, deductibles, provider networks, and prescription coverage together. Using a comparison platform or licensed marketplace such as AHiX Marketplace, can make it easier to review multiple plan options in one place and see how costs differ.

The key takeaway is that COBRA is not your only path. Exploring these options can help you find coverage that better matches your healthcare needs and current budget.

If you want to compare ACA plans side-by-side (premium, deductible, network), AHiX Marketplace can help you review options in one place.

COBRA vs Marketplace Plans – A Cost Comparison

When deciding between COBRA and a marketplace plan, cost is often the biggest concern. Below is a side-by-side comparison to help you understand how COBRA health insurance cost compares with marketplace options.

| Factor | COBRA Coverage | Marketplace Plan (ACA) |

| Monthly Premium | Usually high because you pay the full employer plan cost | Often lower if you qualify for income-based subsidies |

| Employer Contribution | None you pay 100% of the premium | Not needed; financial help may come from tax credits |

| Financial Assistance | No income-based discounts | Premium tax credits based on income and household size |

| Coverage Level | Same plan you had through your employer | Varies by plan tier (Bronze, Silver, Gold, Platinum) |

| Doctor Network | Same doctors and hospitals as before | Network may be different depending on the plan |

| Deductible Status | May continue from current plan year | Usually resets with the new plan |

| Plan Flexibility | Limited to your former employer’s plan | Multiple insurers and coverage levels to choose from |

| Best For | Short-term continuity of care | Long-term affordability and cost control |

This comparison shows why many people exploring alternatives to COBRA insurance look closely at marketplace plans. While COBRA offers stability, marketplace coverage can sometimes reduce monthly costs, especially for households that qualify for financial assistance.

Key Questions to Ask Before Choosing COBRA or Another Plan

Before deciding whether to keep COBRA or switch to another option, it helps to step back and look at your situation from both a medical and financial perspective. Asking the right questions can make the difference between overpaying and finding coverage that truly fits your needs.

Here are important questions to consider:

- How long will I need health coverage?

If you expect to start a new job with benefits soon, paying the COBRA health insurance cost for a short period might make sense. For longer gaps, a lower-cost option may be more practical. - Have I already met my deductible this year?

Staying on COBRA may help you avoid starting over with a new deductible, which can matter if you’ve already had major medical expenses. - Do I expect high medical costs in the near future?

Upcoming surgeries, specialist visits, or ongoing treatments may make keeping the same coverage more convenient. - Can I realistically afford the monthly premium?

Compare the COBRA insurance cost to your current income and other essential expenses. If it strains your budget, exploring alternatives could provide relief. - Do I qualify for income-based savings?

Marketplace plans may offer financial assistance that COBRA does not. This is an important factor when comparing COBRA vs marketplace insurance. - Are my doctors and prescriptions covered under other plans?

Check provider networks and drug coverage before switching so you don’t face unexpected changes in care or medication costs.

Taking time to answer these questions can help you make a more confident decision, rather than choosing coverage based only on urgency or familiarity.

Conclusion: Don’t Assume COBRA Is Your Only Choice

The COBRA health insurance cost can feel overwhelming, especially during a time when income may already be uncertain. While COBRA offers the comfort of keeping the same coverage, it also means paying the full price of an employer plan on your own. For some people, that short-term stability is worth the expense. For many others, it becomes clear that the COBRA insurance cost is simply too high to maintain for long.

The good news is that COBRA is not your only option. Marketplace plans, Medicaid, or coverage through a spouse’s employer may provide more affordable paths to staying insured. Comparing premiums, deductibles, provider networks, and financial assistance opportunities can help you find coverage that better matches both your health needs and your budget.

Before committing, take time to review your situation carefully and explore all available choices. Understanding why COBRA costs so much and what alternatives exist puts you in a stronger position to choose coverage that works for your next chapter.

FAQs

1. How do I sign up for COBRA health insurance?

After your job-based coverage ends, your employer or plan administrator must send you a COBRA election notice. You have 60 days to choose coverage. To enrol, you complete the election form and return it by the deadline. Your coverage will then continue under COBRA once you make your first premium payment.

2. How does COBRA work if I quit my job?

If you quit your job voluntarily, you usually still qualify for COBRA as long as the employer offers group health insurance and you were covered before leaving. You can keep the same plan, but you must pay the full premium yourself.

3. How long can you be on COBRA health insurance?

In most cases, COBRA coverage lasts up to 18 months after job loss or reduced work hours. Some situations allow extensions to 29 months for disability or 36 months for certain family members after qualifying events like divorce.

4. Is COBRA health insurance good coverage?

COBRA coverage is the same health plan you had through your employer, so benefits, doctor networks, and prescription coverage usually remain the same. The main downside is the higher monthly cost.

5. Is there a cheaper alternative to COBRA?

Yes. Many people find marketplace (ACA) plans more affordable because they may qualify for income-based premium tax credits. Medicaid or a spouse’s employer plan can also be lower-cost options.

6. How much does COBRA typically cost per month?

The COBRA health insurance cost often ranges from $400 to $700 per month for individuals and $1,000 to $1,800 or more for families. Costs vary depending on the original employer plan and location.

7. Can I use COBRA for just one month?

Yes. You are not required to keep COBRA for the full eligibility period. You can use it for a short time, such as one month, if you need temporary coverage between jobs or plans.

8. Can I cancel COBRA after one month?

Yes. You can cancel COBRA at any time. Once you cancel, coverage usually ends permanently, and you may need to wait for a Special Enrollment Period or Open Enrollment to get other coverage.

9. How do I find out how much COBRA will cost me?

Your COBRA election notice will list the exact monthly premium. You can also ask your employer’s benefits department or plan administrator for a breakdown of the COBRA insurance cost.

10. Do I have to pay for COBRA if I don’t use medical services?

Yes. COBRA premiums must be paid each month to keep coverage active, even if you do not use healthcare services during that time.

11. What happens if I miss a COBRA payment?

COBRA plans usually offer a short grace period, but if you fail to pay by the deadline, your coverage can be terminated and may not be reinstated.

12. Does COBRA cover pre-existing conditions?

Yes. Because COBRA continues your existing employer plan, it covers pre-existing conditions the same way your previous coverage did.