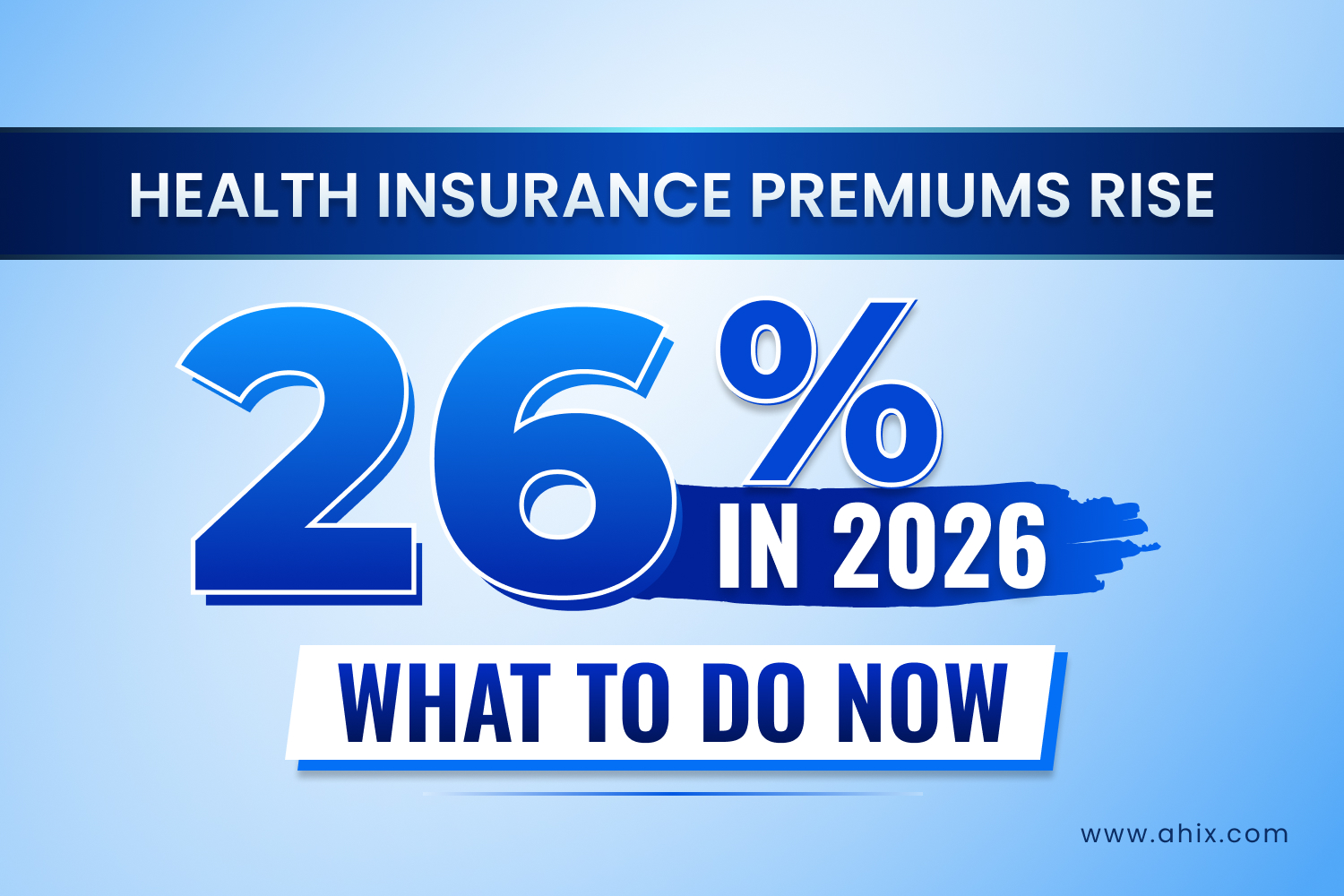

ACA premiums rose an average of 26% in 2026, driven by the expiration of enhanced premium tax credits and rising medical costs. Subsidized enrollees are seeing their out-of-pocket costs jump by an average of 114%. Whether you buy your own plan, get insurance through your employer, or run a small business, this guide covers your exact options ranked by situation

Why Did Health Insurance Go Up So Much in 2026?

If you opened your 2026 health insurance renewal notice and felt a jolt of sticker shock, you are not alone. More than 22 million Americans are experiencing the same thing. Three separate forces collided at the start of 2026 to create the largest premium spike since 2018, and understanding all three is the first step to doing something about it.

The Enhanced Premium Tax Credits Expired

This is the biggest driver for buyers of marketplace plans. From 2021 through 2025, during the COVID-era, the American Rescue Plan Act and the Inflation Reduction Act provided tens of millions of Americans with extra government subsidies to lower their monthly premiums. These “enhanced” premium tax credits expanded who qualified and increased how much financial help eligible households received.

Congress let them expire on December 31, 2025.

The impact is staggering. According to KFF, subsidized enrollees are seeing their out-of-pocket premium payments increase by an average of 114% in 2026. That is not a typo. A single person earning $28,000 per year, who paid $325 annually for a benchmark silver plan under the enhanced credits, now pays approximately $1,562, an increase of $1,237 in a single year. A lower-income individual earning $22,000, who previously paid $0 per month, now pays $66 monthly just to maintain the same coverage.

For people at or above 400% of the federal poverty level ($62,600 for a single person; $128,600 for a family of four), the situation is sharper still: they no longer qualify for any premium tax credit at all, meaning they absorb both the lost subsidy and the underlying rate increase simultaneously.

Healthcare Costs Themselves Are Climbing

Even setting aside the subsidy expiration, insurers are raising rates because the underlying cost of care keeps going up. Hospital admissions, physician services, and prescription drug costs are all trending upward at roughly 8% annually, according to insurer rate filings analyzed by the Peterson-KFF Health System Tracker.

A specific accelerant: GLP-1 medications like Ozempic and Wegovy. These drugs, prescribed for diabetes and weight loss, carry price tags of $900 to $1,400 per month. As more Americans use them and insurers cover them, the cost pressure on every premium-paying member increases.

Insurers Are Pricing In the People Who Will Leave

There is a compounding effect that most people don’t realize. When subsidies expire, the healthiest and youngest enrollees who are the most price-sensitive and least dependent on coverage are also the most likely to drop their plans. Insurers know this. They have priced 2026 premiums accordingly, raising rates an extra 4 percentage points on average to account for the sicker risk pool they expect to be left with. The net result: premiums rise, healthy people leave, premiums rise further. It is a cycle that makes acting sooner rather than later financially important.

How Much Did Premiums Actually Increase? (By State and Situation)

For designer: banner image with text: Premium Increase Breakdown (By State & Situation)

The national averages are alarming enough. But your actual premium change depends heavily on your state, your income, your age, and what plan you are on.

National Averages

ACA Marketplace insurers raised their gross premiums by an average of 26% in 2026, according to KFF analysis of finalized rate filings. For the benchmark silver plan (second-lowest cost silver), which drives subsidy calculations:

- States using Healthcare.gov (federally-facilitated exchange): benchmark silver premiums up 30%

- States running their own exchanges (New York, Massachusetts, California, Maryland): more moderate increases, typically 10–17%, due to community rating rules and state-level assistance programs

Employer-sponsored plans are faring better by comparison. The total health benefit cost per employee rose approximately 6.5% on average in 2026, the highest increase since 2010, according to Mercer’s National Survey of Employer-Sponsored Health Plans, but still far below what marketplace buyers are experiencing.

By Situation: What Are You Actually Paying?

| Your Situation | 2025 Monthly Premium | 2026 Monthly Premium | Change |

| Individual, $22K income, subsidized ACA plan | $0/month | $66/month | New cost |

| Individual, $28K income, subsidized ACA plan | ~$27/month | ~$130/month | +114% |

| Individual, $50K income, ACA marketplace | ~$180/month | ~$250/month | +39% |

| Individual, 60 years old, above 400% FPL | ~$500/month | ~$850+/month | +70%+ |

| Employee on employer plan (individual) | varies | +6–7% paycheck deduction | Mercer data |

| Small business group plan (employer cost) | varies | +11% median | KFF data |

States Getting Hit Hardest

States that use Healthcare.gov and have less competitive insurance markets are seeing the largest premium jumps. Pennsylvania, for example, saw insurers request an average 19% increase in the individual market and 13% in the small group market, with some carriers like Ambetter requesting increases as high as 30.1%. Insurers in states with fewer competitors have less pressure to hold rates down.

States with their own exchanges and additional state subsidies, such as California, New York, Maryland, and Massachusetts, are providing meaningful cushions. Covered California, for instance, committed to automatically applying any restored federal credits and maintaining state-level support. If you live in one of these states, check your state exchange directly for local assistance programs that may not appear on Healthcare.gov.

What This Means for YOUR Specific Situation

The most important thing to understand is that 2026’s premium increase is not a single story. It affects different people in fundamentally different ways, and the right response depends entirely on which situation you are in.

You Buy Your Own ACA Marketplace Plan

You are feeling the most acute pain. The 114% average increase for subsidized enrollees is largely your story. Your immediate priorities are:

First, re-run your subsidy calculation. Your subsidy eligibility is based on your current-year income, not last year’s. If your income dropped, you may qualify for more help than your original enrollment estimated. Use the KFF ACA Subsidy Calculator (kff.org) to check.

Second, check Medicaid eligibility. If your household income is at or below 138% of the federal poverty level ($20,783 for a single person in 2026), you may qualify for Medicaid, which has no premium at all. Many people who were just above the Medicaid threshold under the enhanced credits are now below it.

Third, consider whether a Bronze or Catastrophic plan fits your situation better than your current plan. See the section below on how to make that trade-off.

Your Employer Covers You

You are insulated from the worst of this, but not untouched. The 6.5% average employer cost increase will translate to approximately 6–7% higher paycheck deductions for employee premiums. More significantly, many employers are responding by raising deductibles, increasing copays, and narrowing provider networks to absorb the overall cost increase.

Check your 2026 plan documents specifically for: your new deductible amount, your new out-of-pocket maximum, and whether your preferred doctors are still in-network. If your deductible jumped significantly, a supplemental accident or hospital indemnity plan (typically $30–$80/month) can close that gap without switching your primary coverage.

You Are a Small Business Owner or Employer

You are caught between two pressures: a median 11% group plan premium increase from your carrier, and employees who are watching their paycheck deductions grow. According to Mercer, 59% of employers are making cost-cutting changes to plans in 2026, up from 48% in 2025. Raising deductibles is the most common move. But there is a more strategic option.

An ICHRA (Individual Coverage Health Reimbursement Arrangement) lets you set a fixed monthly allowance per employee, say, $400/month, and employees use that money to shop for their own ACA-compliant plans. Your cost is exactly what you set it to be. No carrier renewal negotiations. No surprise rate hikes. And employees can often find individual plans that cost them less than a group plan would have, because they can shop the full marketplace and apply any subsidies they qualify for independently.

For a business with 10 employees at a $400/month ICHRA allowance, your total monthly health benefit cost is exactly $4,000. That number does not change unless you choose to change it.

You Are Self-Employed or a Freelancer

You are absorbing the full premium increase with no employer contribution to cushion it. The good news: your health insurance premiums are 100% tax-deductible if you are self-employed, which means the real after-tax cost is meaningfully lower than the sticker price. A person in the 22% federal tax bracket paying $500/month in premiums has an effective net cost of $390/month after the deduction.

Beyond the deduction, the most powerful tool available to you is reducing your adjusted gross income (AGI) to stay under key subsidy thresholds. Every dollar you contribute to a traditional IRA or Solo 401(k) reduces your MAGI, the income figure used to calculate your subsidy. At the 400% FPL threshold ($62,600 for an individual), a $5,000 IRA contribution can mean the difference between qualifying for thousands of dollars in premium tax credits and receiving nothing.

You Are Approaching Medicare Age (55–64)

This group is absorbing the largest dollar increases of any demographic. A 62-year-old above 400% FPL can easily be looking at $850 to $1,200 per month for marketplace coverage in 2026, up from $500–$700 in 2025. The options are limited but real: assess whether any part-time work provides access to employer coverage, evaluate COBRA if you recently left a job, and consider whether a catastrophic plan under the CMS hardship exemption covers your minimum needs while you bridge to Medicare at 65.

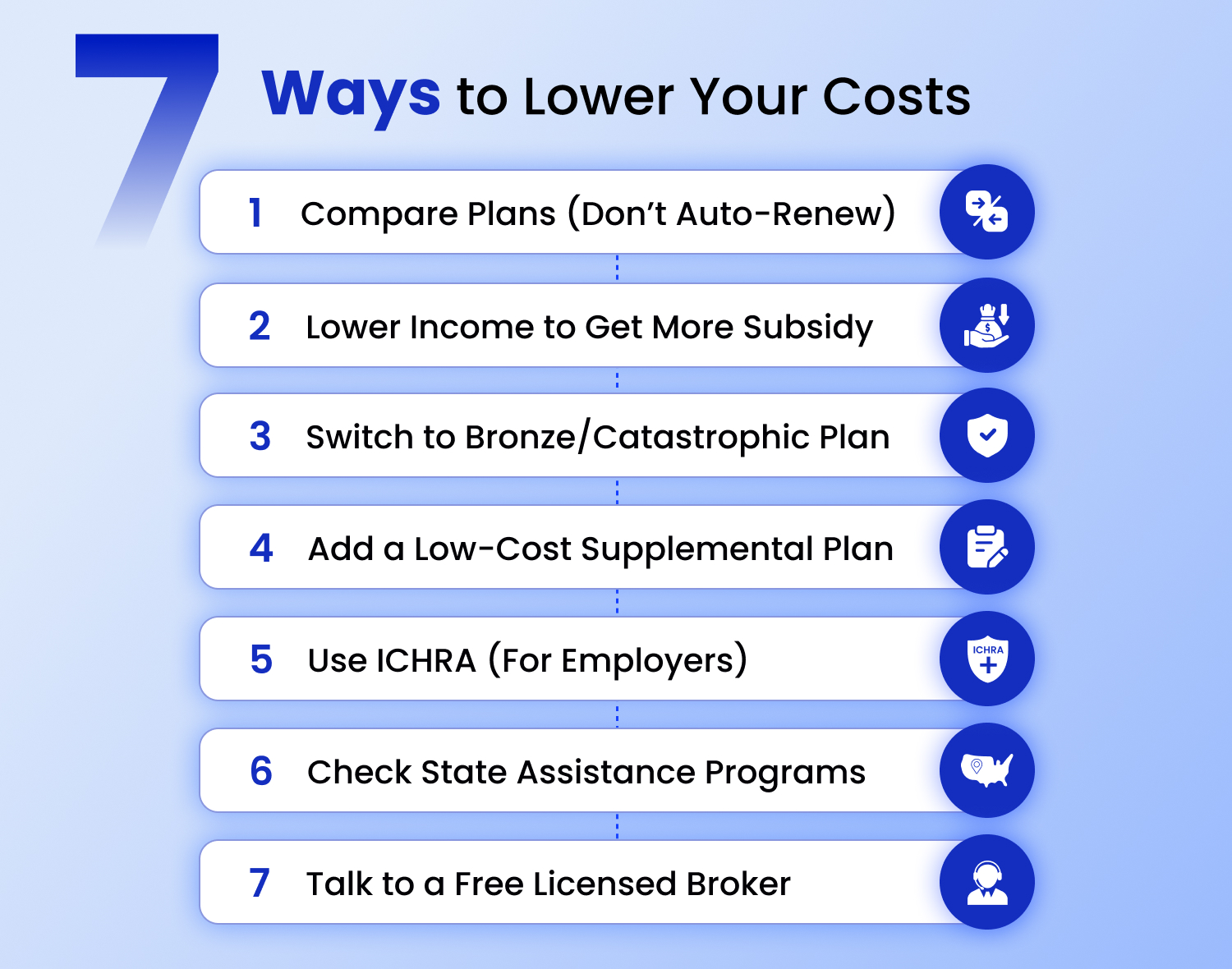

7 Ways to Lower Your Health Insurance Cost Right Now

Here are the seven most effective strategies, ranked from broadest applicability to most targeted. Most people can use at least three of these.

1. Re-Shop Your Plan. Do Not Auto-Renew

This is the single most universally impactful action you can take, and the most commonly skipped. Auto-renewal locks you into your current plan even if cheaper or better-suited options have entered your market.

The cheapest silver plan in your county may have changed. New insurers may have entered your market. Your doctors’ network affiliations may have shifted. Spending 20 minutes comparing plans on Healthcare.gov or through an AHiX licensed agent can surface savings of $500 to $2,000 annually for many people. Do this before accepting your renewal notice as final.

2. Reduce Your AGI to Maximize Subsidy Eligibility

If you are near a key income threshold, particularly the 400% FPL cutoff or the Medicaid eligibility line, reducing your modified adjusted gross income can unlock significant savings.

The most effective tools:

- Traditional IRA contributions: Up to $7,000 ($8,000 if 50+) directly reduces your MAGI

- HSA contributions: $4,300 for individual coverage, $8,550 for family coverage in 2026, fully deductible and usable for qualified medical expenses

- Solo 401(k) or SEP-IRA (self-employed): Contributions can be $10,000 to $23,000+, creating substantial MAGI reduction

- Health FSA through employer: Pre-tax contributions reduce your taxable income

Important note: The 400% FPL cutoff is a hard cliff under the restored pre-2021 rules. A single dollar above it eliminates your entire premium tax credit. For a family of four, that threshold is $128,600. If you are near it, aggressive retirement account contributions are not just good financial planning; they are direct healthcare cost reduction.

3. Switch to a Bronze or Catastrophic Plan if You Are Generally Healthy

Gold and silver plans make sense if you use healthcare frequently. If you are healthy, rarely see doctors beyond annual preventive visits, and primarily need insurance for financial catastrophe protection, a Bronze plan or catastrophic plan can be dramatically cheaper.

Catastrophic plans were expanded in 2026 via CMS hardship exemption guidance, specifically because of the premium surge. They cover all essential health benefits and provide full preventive care at no cost but carry a deductible of approximately $9,450 before other benefits kick in. For a 32-year-old in good health, a catastrophic plan at $80–$120/month may be a far better financial decision than a Silver plan at $280/month.

The math to evaluate: multiply the premium difference by 12, then compare to the deductible gap. If switching from Silver to Catastrophic saves you $160/month ($1,920/year) but raises your deductible by $6,000, you come out ahead in any year you do not hit that deductible, which, statistically, is most years for healthy people under 40.

4. Stack a Supplemental Plan Instead of Upgrading Your Primary

Supplemental health insurance accident plans, critical illness plans, and hospital indemnity plans work alongside your primary coverage to cover what it does not. These plans typically cost $30 to $80 per month and pay cash benefits for specific events: an ER visit, a broken bone, a cancer diagnosis, and a hospital admission.

If your primary plan raised its deductible from $1,500 to $3,500 this year, an accident plan that pays $2,000 per accident at $45/month ($540/year) is almost certainly worth it. You are paying $540 to cover a $2,000 gap in a straightforward trade. This strategy keeps your primary plan costs down while closing the gaps created by higher deductibles.

5. Employers: Switch to ICHRA and Lock In Your Budget

If you are a small business owner currently renewing a group health plan, this is the year to seriously evaluate the ICHRA alternative. Your group plan’s carrier sets your premium. With ICHRA, you set your budget, and it never changes unless you choose to change it.

The mechanism is simple: you define a monthly reimbursement allowance for each employee class (full-time, part-time, etc.), employees shop the marketplace for a plan that fits their needs, they pay their premium directly, and you reimburse them up to the allowance, tax-free. Your cost per employee is exactly your allowance amount. Nothing more, ever.

For a 15-person business facing an 11% group plan renewal increase, switching to ICHRA with a $450/month allowance per full-time employee costs $6,750/month, a number that stays fixed regardless of what carriers do next year.

6. Check State-Specific Assistance Programs

Several states have maintained or expanded their own subsidy programs independent of the federal enhanced credits that expired. If you live in one of these states, you may qualify for additional financial assistance that does not appear automatically:

- California (Covered California): State-level subsidies remain in place; some lower-income enrollees continue to pay $10/month or less

- New York: Community-rated premiums limit age-based variation; Essential Plan covers those under 200% FPL at no cost

- Massachusetts: ConnectorCare program provides state subsidies to residents under 300% FPL

- Maryland, Washington, and Minnesota: Each has additional state assistance programs worth checking

Visit your state’s official exchange website directly, not just Healthcare.gov, to see all available assistance programs in your state.

7. Work With a Licensed Broker. It Costs You Nothing

Insurance brokers are compensated by the insurance carriers, not by you. Their services include plan comparison, subsidy calculation, enrollment assistance, and claims help, costing you zero out of pocket. And a skilled broker can find plan combinations, subsidy strategies, and supplemental pairings that the general marketplace interface does not surface.

This is especially valuable if your situation is complex: if you are self-employed with variable income, if you are transitioning off an employer plan, if you are comparing COBRA to marketplace options, or if you need to coordinate coverage for a family with different healthcare needs. A 30-minute conversation with a licensed agent can identify savings opportunities that take minutes to implement.

Should You Drop Your Health Insurance Altogether in 2026?

The Urban Institute and Commonwealth Fund project that 4.8 million Americans will drop their health coverage in 2026 as a direct result of the premium increases. That is an understandable response to a bill that doubled overnight. But it is also one of the most financially dangerous decisions most people will ever make.

The federal individual mandate penalty no longer applies; you will not be fined for going uninsured. But the financial exposure is significant. Consider what you are actually absorbing as financial risk by going uninsured:

- Average emergency room visit: $2,200 without insurance

- Broken arm requiring surgery: $16,000–$25,000

- Appendectomy: $33,000 average

- 3-day hospital stay for any cause: $30,000 average

- Cancer diagnosis and initial treatment: $150,000+

A catastrophic plan at $80–$130/month costs roughly $1,000–$1,500 per year. A single emergency room visit without insurance costs more than that. The math on going completely uninsured rarely works out, even for young and healthy people. The question is not whether to have insurance but which combination of coverage and cost is right for your situation.

Will the ACA Subsidies Come Back in 2026?

As of April 2026, the enhanced premium tax credits remain expired. Here is the current political situation in plain terms:

The enhanced credits expired on December 31, 2025, after Congress failed to pass an extension. In December 2025, the Senate rejected two partisan bills: a Democratic proposal to extend credits for three years and a Republican alternative focused on health savings accounts. Four centrist House Republicans joined Democrats to push for a floor vote on a three-year extension, but as of this writing, no extension has passed.

The Congressional Budget Office estimates that a permanent extension would cost approximately $350 billion over ten years, a figure that has made it difficult to pass in the current fiscal environment. Budget negotiations are ongoing.

What you should do: Plan your 2026 healthcare budget as if the enhanced credits will not return this year. If they do come back, any marketplace changes would be applied automatically, and you would receive a notice to adjust your plan if desired. Planning for the worst outcome and being pleasantly surprised is a far better position than budgeting for restored subsidies that may not materialize.

Frequently Asked Questions

Why did my health insurance premium go up so much in 2026?

Your premium increased primarily because enhanced ACA premium tax credits expired on December 31, 2025. These credits have lowered out-of-pocket costs for 22 million Americans since 2021. Without them, subsidized enrollees are paying an average of 114% more, while insurers also raised gross premiums by 26% on average due to rising healthcare costs and GLP-1 drug expenses.

Did the ACA subsidies expire in 2026?

Yes. The enhanced premium tax credits, which had been in effect since 2021 under the American Rescue Plan Act and extended by the Inflation Reduction Act, expired December 31, 2025. Basic premium tax credits still exist for lower-income individuals, but the enhanced amounts that benefited middle-income households are gone unless Congress acts to restore them.

How much did health insurance premiums increase in 2026?

ACA Marketplace gross premiums rose an average of 26% in 2026. For subsidized enrollees, the out-of-pocket increase is far higher, an average of 114%, because they are absorbing both the rate increase and the loss of enhanced subsidies simultaneously. Employer-sponsored plan costs rose approximately 6.5%, the highest increase since 2010.

What is the cheapest health insurance option in 2026?

For lower-income individuals (under 138% FPL), Medicaid remains the lowest-cost option — often free. For those with incomes 138–250% FPL, subsidized Bronze plans can still be very affordable. For healthy individuals under 30, Catastrophic plans are the lowest-premium option with full essential health benefits. For small businesses, ICHRA with a modest allowance provides a budget-controlled option without group plan minimums.

Can I get health insurance without a subsidy in 2026?

Yes. You can purchase any ACA-compliant plan directly through Healthcare.gov or through a private marketplace like AHiX without receiving a subsidy. You will pay the full gross premium, which averages 26% higher than last year, but you retain all plan benefits and ACA protections, including coverage for pre-existing conditions.

How does ICHRA help employers deal with premium increases?

An ICHRA (Individual Coverage Health Reimbursement Arrangement) allows employers to set a fixed monthly reimbursement allowance per employee instead of buying a group plan. Because the employer’s cost is defined by the allowance they set, not by a carrier’s premium there are no surprise renewal increases. If a carrier raises rates, that affects the employee’s plan choice, not the employer’s budget.

What is a catastrophic health plan, and who qualifies in 2026?

A Catastrophic plan covers all essential health benefits with a high deductible (approximately $9,450 in 2026) and lower monthly premiums. You normally qualify if you are under 30. In 2026, CMS expanded hardship exemption eligibility specifically because of the premium surge, allowing more people to access Catastrophic plans even if they are over 30 and facing significant affordability challenges.

Can I still change my health insurance plan in 2026?

Outside of Open Enrollment (November 1 – January 15), you can only change plans if you qualify for a Special Enrollment Period (SEP). Qualifying life events include losing other coverage, getting married or divorced, having a baby, moving to a new coverage area, and changes in income that affect your subsidy eligibility. Contact an AHiX licensed agent to determine whether your situation qualifies for an SEP.

Is it worth having health insurance if premiums doubled?

For most people, yes. A single emergency room visit without insurance costs more than a year of catastrophic plan premiums. The question is not whether to be insured, but which level of coverage is right for your health needs and budget. A catastrophic or bronze plan at a lower premium is far better protection than no coverage at all.

What states have additional help beyond federal subsidies in 2026?

California, New York, Massachusetts, Maryland, Washington, and Minnesota all have state-level programs that provide additional financial assistance beyond federal premium tax credits. Residents of these states should check their state exchange website, not just Healthcare.gov to see all available assistance.

The Bottom Line

Your premiums went up. Your options did not disappear.

Whether you need to re-shop your marketplace plan, reduce your AGI to restore subsidy eligibility, switch to a Bronze or Catastrophic plan, explore ICHRA for your employees, or simply talk through your situation with someone who understands every option, the right move is to act now rather than accept a renewal that may not reflect your best available option.

At AHiX Marketplace, our licensed agents help individuals, families, and small business owners find the right coverage at the right price using direct carrier feeds that reflect real 2026 pricing across every available plan in your area. There is no charge to compare plans or speak with an agent.