You work 25 hours a week. You show up, get the job done, and genuinely love what you do. But when you got sick last month, there was no employer plan to fall back on, you paid every single dollar out of pocket. Sound familiar?

You’re not alone. Only 19% of part-time workers in the U.S. are covered by their own employer’s health plan. That means the vast majority of the country’s 26+ million part-time workers are left to navigate the insurance market on their own, often without knowing what options are actually available to them.

This guide cuts through the confusion. You’ll learn exactly what the law says about employer coverage obligations, what your real alternatives are, how much you’ll likely pay, and how to find a plan that fits your life without needing an employer to make it happen.

AHiX connects part-time workers directly to health plans from real, licensed carriers, no employer required, no sales pressure, no runaround. You can compare real plans in your ZIP code in under 5 minutes.

Can Part-Time Employees Get Health Insurance From Their Employer?

This is the question most part-time workers start with and the answer is: it depends, but usually no. Here’s what the law actually says and when employer coverage might still be on the table.

What the Law Actually Says: The ACA 30-Hour Rule

Under the Affordable Care Act, an employee is classified as part-time if they average fewer than 30 hours per week or 130 hours per month. For employers with 50 or more full-time equivalent employees, known as Applicable Large Employers (ALEs) the ACA’s employer mandate only requires them to offer health insurance to full-time workers. Part-timers are legally excluded.

In plain terms: if you work under 30 hours per week, your employer has zero legal obligation to offer you health coverage, regardless of how long you’ve been there or how important your role is.

This catches a lot of part-time workers off guard. Many assume that loyalty or tenure earns them benefits. The law, unfortunately, doesn’t see it that way.

When Employers Do Offer Part-Time Coverage

Some employers, often larger companies competing for talent, voluntarily extend health benefits to part-time staff. Retailers like Costco, Starbucks, and some healthcare systems have been known to offer coverage to employees working as few as 20 hours per week.

If you’re unsure whether your employer offers this, ask HR directly and review your employee handbook. One important legal nuance worth knowing: if your employer does offer coverage to part-timers, they must offer it consistently to all similarly situated employees. They cannot cover one part-timer and deny the same benefit to another person doing the same job at the same hours.

If coverage isn’t available through your job, don’t stop there. The marketplace has strong options, and many part-time workers actually pay less for individual coverage than they expect.

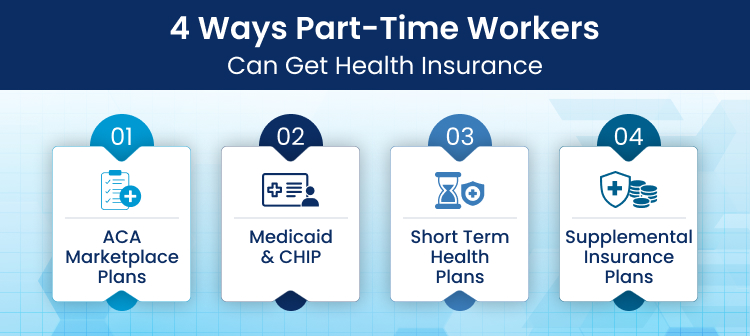

Health Insurance Options for Part-Time Workers Without Employer Coverage

Not having employer-sponsored health insurance doesn’t mean going without. Part-time workers actually have access to several solid coverage pathways, and depending on your income, you may qualify for significant financial help.

ACA Marketplace Plans | The Most Popular Option

The Health Insurance Marketplace, created by the Affordable Care Act, was built specifically for people who don’t have job-based coverage. Part-time workers are a primary target audience, and the plans available are comprehensive.

Every ACA plan covers pre-existing conditions from day one with no waiting periods, no exclusions. Plans are offered in four metal tiers (Bronze, Silver, Gold, Platinum), giving you control over how you balance your monthly premium against your out-of-pocket costs.

Critically, many part-time workers qualify for premium tax credits (subsidies) that significantly reduce monthly costs. A 35-year-old earning $30,000 per year could pay as little as $0–$80/month after subsidies, depending on their state and plan tier.

You can enroll during Open Enrollment (November 1 – December 15) or during a Special Enrollment Period if you’ve had a qualifying life event like losing coverage, moving, getting married, or having a child.

Medicaid & CHIP | Free or Very Low Cost If You Qualify

If your income falls below a certain threshold, you may qualify for Medicaid, a government-funded program that offers free or near-free health coverage. In states that expanded Medicaid under the ACA, a single adult earning up to about $20,120/year may qualify.

It’s worth knowing: part-time workers are significantly more likely to be covered by Medicaid (21%) than their full-time counterparts (7%). If your income is modest, this is worth checking before paying for a marketplace plan.

CHIP (Children’s Health Insurance Program) covers low-income children and, in some states, pregnant women, another option for part-time working parents.

Short-Term Health Plans | The Stop-Gap Solution

Short-term health plans are flexible, lower-premium plans designed to bridge coverage gaps, for example, between jobs, while waiting for Open Enrollment to start, or during a period of transition.

These plans are not ACA-compliant, which means they don’t cover pre-existing conditions and benefits are more limited. However, for a healthy individual who primarily needs protection against unexpected emergencies, a short-term plan can deliver real value at a much lower monthly cost.

AHiX offers a range of short-term plans from licensed carriers so you can compare options and make an informed choice.

Supplemental Plans | Fill the Gaps Your Primary Plan Leaves Behind

Even with a solid primary plan, out-of-pocket costs can add up fast. Supplemental plans, including accident coverage, critical illness insurance, and hospital indemnity plans, pay you directly when certain events occur, filling in the gaps your primary coverage doesn’t address.

These are particularly valuable for part-time workers who opt for a high-deductible ACA plan to keep premiums low. A supplemental accident plan, for example, can cover your deductible if you end up in the ER after an injury. AHiX offers a curated selection of supplemental options that pair seamlessly with marketplace plans.

Plan Comparison: Which Option Is Right for You?

Choosing the right coverage depends on your income, health needs, and how long you need coverage. Here’s a side-by-side breakdown to help you decide:

| Plan Type | Best For | Est. Monthly Cost | Pre-Existing Conditions | Where to Get It |

| ACA Marketplace Plan | Most part-time workers | $0–$400/mo (subsidies available) | Fully Covered | AHiX / Healthcare.gov |

| Medicaid | Lower-income workers | Free – very low cost | Fully Covered | Healthcare.gov |

| Short-Term Plan | Temporary gap coverage | $50–$150/mo | Usually Excluded | AHiX |

| Supplemental Plan | Add-on protection | $20–$80/mo | Varies by plan | AHiX |

| Employer Group Plan | Workers at 20–30+ hrs/week | Employee share only | Covered | Through your employer |

💡 Pro Tip: Many part-time workers combine an ACA plan with a supplemental plan for the most complete coverage at the lowest total cost. AHiX lets you compare both side by side.

Not sure which plan fits your situation? Compare real plans on AHiX in 3 minutes

How to Get Health Insurance as a Part-Time Worker: A Step-by-Step Guide

This is the section most health insurance articles skip entirely. Here’s exactly what to do in order to get yourself covered:

- Check whether your employer offers any part-time coverage. Ask HR or check your employee handbook. Even partial coverage may be worth taking if the employer contributes to the premium.

- Estimate your annual household income. This single number determines whether you qualify for Medicaid (free), ACA subsidies (discounted plans), or full-price marketplace coverage.

- Identify your coverage priority. Do you need comprehensive ACA coverage with pre-existing condition protection? Or are you healthy and mainly need a stopgap short-term plan?

- Browse and compare plans on AHiX. Enter your ZIP code, income, and basic health info to see real plans, real prices, and real carrier details, no sign-up required to browse.

- Enroll during Open Enrollment (Nov 1–Dec 15) or apply during a Special Enrollment Period. You qualify for a Special Enrollment Period if you’ve experienced a qualifying life event see the list below.

Qualifying Life Events That Trigger a Special Enrollment Period

- Losing job-based health coverage (including reduction to part-time hours)

- Moving to a new ZIP code or county

- Getting married or divorced

- Having a baby, adopting a child, or placing a child for foster care

- A change in household income that affects your subsidy eligibility

- Gaining citizenship or lawful presence in the U.S.

How Much Does Health Insurance Actually Cost for Part-Time Workers?

This is the question that stops most part-time workers from even starting the search, and the answer is almost always better than expected. Here’s why.

The Subsidy Advantage Most Part-Timers Don’t Know About

Under the ACA, premium tax credits (subsidies) are available to individuals and families earning between 100% and 400% of the Federal Poverty Level (FPL). In many states, those earning up to 600% FPL can still receive some assistance.

What this means in practice: a single adult earning $25,000/year could pay as little as $0–$60/month for a Silver plan after subsidies. At $35,000/year, that estimate rises to roughly $80–$150/month still far less than most part-time workers assume.

Critical point: many part-time workers who’ve assumed they can’t afford coverage are actually entitled to premium tax credits they’ve never claimed. The only way to know what you’ll pay is to check.

Real Cost Example

| Profile | Annual Income | Est. Monthly Premium (After Subsidy) | Plan Type |

| Single adult, age 28 | $22,000/year | $0 – $40/mo | Silver ACA Plan |

| Single adult, age 35 | $30,000/year | $50 – $100/mo | Silver ACA Plan |

| Single parent, 1 child, age 32 | $28,000/year | $30 – $80/mo | Silver ACA Plan |

| Single adult, age 45 | $40,000/year | $130 – $200/mo | Silver ACA Plan |

Note: Estimates vary by state and carrier. Actual premiums shown on AHiX reflect your exact ZIP code and plan options.

Frequently Asked Questions

1. Can part-time employees buy health insurance through the marketplace?

Yes absolutely. The ACA Marketplace was designed specifically for people who don’t have job-based coverage. Part-time workers can shop, compare, and enroll in plans directly, and many qualify for subsidies that significantly reduce monthly costs. AHiX makes this process faster by showing you real plans in your area in minutes.

2. How many hours do you have to work to qualify for employer health insurance?

Under the ACA, employers are only required to offer coverage to employees averaging 30 or more hours per week (or 130 hours per month). Employers with fewer than 50 full-time equivalent employees have no mandate at all, regardless of hours. If you fall below these thresholds, individual marketplace coverage is your primary path.

3. What if I work two part-time jobs can I still get coverage?

Yes. ACA Marketplace eligibility is based on your total household income, not which employer you work for. As long as neither job offers affordable, adequate coverage, you can shop the marketplace independently and may qualify for subsidies based on your combined income.

4. Can gig workers and freelancers get health insurance as part-time workers?

Yes. The ACA Marketplace treats self-employed, gig, and freelance workers the same as part-time employees. Your eligibility is income-based, not employment-status-based. Many gig workers also qualify for significant subsidies, especially if their income fluctuates.

5. When can I enroll if I don’t have employer coverage?

You can enroll during the annual Open Enrollment Period, which runs from November 1 to December 15 each year (coverage begins January 1). If you experience a qualifying life event such as losing coverage, moving, or having a life change you qualify for a Special Enrollment Period that opens a 60-day window to enroll outside the standard schedule.

6. What is the difference between a short-term plan and an ACA marketplace plan?

ACA marketplace plans are comprehensive, cover pre-existing conditions from day one, and are eligible for government subsidies. Short-term plans are less expensive but more limited; they typically exclude pre-existing conditions and offer fewer benefits overall. Short-term plans work best as temporary stop-gap coverage; ACA plans are the better long-term solution for most part-time workers.

The Bottom Line: You Have More Options Than You Think

Remember that feeling at the start, paying out of pocket because you assumed coverage wasn’t available to you? That assumption costs part-time workers thousands of dollars every year in unnecessary medical bills.

Here’s the core truth: part-time workers in the U.S. have real, affordable health insurance options, ACA marketplace plans, Medicaid, short-term coverage, and supplemental plans, and many pay far less than they expect once subsidies are factored in. You don’t need an employer to get covered. You need the right marketplace.

AHiX connects consumers with plans from licensed insurance carriers and brokers, no sales pressure, no confusion. Just clear options, real prices, and a straightforward path to coverage in your ZIP code, for your situation.