When you’re looking for a health insurance plan, you’ll often see terms like premium, copay, and deductible. Out of all these, the health insurance deductible is one of the most important things to understand, yet many people are not sure what it really means or how it works.

At AHiX Marketplace, we believe in helping you understand your health insurance options clearly. Whether you’re buying a plan for yourself or your family, knowing how a deductible affects your costs can help you choose the right plan and avoid surprise medical bills.

In this article, we’ll explain what a health insurance deductible is, how it works in real life, and why it matters when comparing health plans. You’ll also learn how your deductible works with other health costs like premiums, copays, and coinsurance and how to find the right balance for your health and budget.

What Is Health Insurance Deductible?

A health insurance deductible is the amount you must pay for covered medical services each year before your insurance begins to pay its share.

For example, if your deductible is $1,500, you must pay the first $1,500 of your healthcare costs out of your own pocket. After that, your insurance company will begin to help cover future costs according to your plan.

Key Point: Your deductible is separate from your monthly premium. The premium is what you pay each month to have the insurance, while the deductible is what you pay when you need care.

How Does Deductible Insurance Work?

To better understand how a health insurance deductible fits into your overall coverage, let’s walk through the process step-by-step.

- You visit a doctor or need medical treatment.

- If the service is covered by your plan, the bill goes toward your deductible.

- You pay 100% of the allowed cost until your deductible is met — unless your plan includes copays for certain services (like doctor visits or prescriptions), which may apply before you meet your deductible.

- After you’ve paid the full deductible, your insurer starts sharing the costs through coinsurance or copays that didn’t apply before your deductible was met.

If your total spending reaches the out-of-pocket maximum, your insurance covers 100% of eligible costs for the rest of the year.

Here’s a quick overview:

| Cost Term | What It Means |

| Deductible | What you pay before insurance starts helping |

| Premium | What you pay monthly for the insurance plan |

| Copay | A fixed fee you pay when you get specific services |

| Coinsurance | A percentage you pay after the deductible is met |

| Out-of-Pocket Maximum | The maximum amount you’ll pay in one year |

However, many preventive services—like annual checkups, screenings, and vaccines—are covered before the deductible and are often provided at no cost to you.

It’s important to read your plan details or visit AHiX Marketplace to see what services count toward your deductible in each plan you’re considering.

Health Insurance Deductible vs. Premium vs. Copay

These terms often confuse people. Let’s clear it up with a table:

| Term | When You Pay It | What It Covers |

| Premium | Monthly, even if you don’t use services | Keeps your health insurance active |

| Deductible | When you receive medical care | Must be paid before insurance begins sharing costs |

| Copay | At the time of service (in some plans) | Flat fee for specific services like doctor visits |

| Coinsurance | After the deductible is met | You pay a percentage; insurance pays the rest |

Understanding the difference helps you estimate how much you’ll pay over the year.

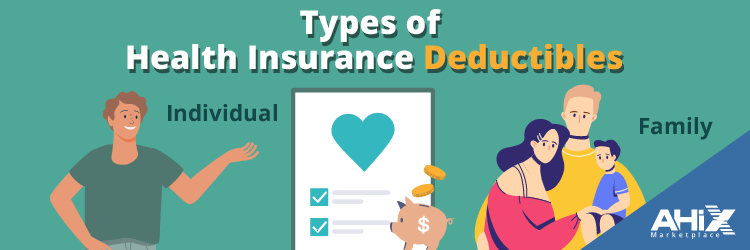

Types of Health Insurance Deductibles

When you choose a health plan, you may see different types of deductibles based on whether the coverage is just for you or for your entire family.

1) Individual Deductible

Applies to a single person on the plan. Once that person meets the deductible, the plan begins to share the cost for that individual’s care.

2) Family Deductible

If you cover more than one person, the plan may offer both individual and family deductibles. Here’s how it works:

- Embedded deductible: Each person has an individual deductible. Once one person meets it, insurance starts paying for that person—even if the family deductible hasn’t been met.

- Non-embedded deductible: The full family deductible must be met before insurance helps with costs for anyone on the plan.

High Deductible vs. Low Deductible Health Plans

When shopping for a health plan on AHiX Marketplace, you’ll often compare high deductible health plans (HDHPs) and low deductible plans. Here’s how they differ:

| Feature | High Deductible Plan (HDHP) | Low Deductible Plan |

| Monthly Premium | Lower | Higher |

| Upfront Medical Costs | Higher | Lower |

| Best for | Healthy people or those who rarely use care | People who expect frequent care |

| HSA-Eligible | Yes, depending on the plan | Usually not |

| Risk Level | More risk if you need care | Less risk, more predictable costs |

If you’re generally healthy and want lower monthly costs, a high deductible health plan may work well. If you expect ongoing treatment, medications, or frequent doctor visits, a low deductible plan may reduce your total spending.

When Is a High Deductible Plan a Good Choice?

A high deductible health plan is a good choice if:

- You want lower monthly premiums.

- You don’t expect to use much healthcare.

- You’re comfortable paying more out of pocket if something unexpected happens.

- You want to open a Health Savings Account (HSA) for tax benefits.

HSAs allow you to save pre-tax dollars for medical expenses, including deductibles, prescriptions, and doctor visits. These funds roll over from year to year and grow tax-free.

When Should You Choose a Low Deductible Plan?

You might prefer a low deductible plan if:

- You or a family member has a chronic condition.

- You visit the doctor or specialists often.

- You want lower costs when you need care—even if monthly premiums are higher.

- You prefer more predictable healthcare expenses throughout the year.

How to Choose the Right Health Insurance Deductible

Here are some tips to help you choose wisely:

- Review your past medical use. Did you visit the doctor often last year? Do you expect surgeries or ongoing prescriptions?

- Look at your budget. Can you afford to pay a higher deductible if something serious happens?

- Compare total yearly costs. Look at the combination of premium + deductible + expected out-of-pocket costs.

- Use comparison tools. On AHiX Marketplace, you can compare plans side-by-side based on deductible, premium, and coverage.

Do Preventive Services Count Toward the Deductible?

Under the Affordable Care Act, most preventive services are covered at no cost to you, even before you meet your deductible. These include:

- Annual wellness exams

- Cancer screenings

- Vaccinations

- Blood pressure and diabetes tests

- Prenatal care

Preventive care can help catch issues early and keep you healthy—without any additional cost.

What Happens After You Reach Your Deductible?

Once you meet your health insurance deductible, your insurance begins to share the cost of services through coinsurance or copays. You will continue cost-sharing until you reach your out-of-pocket maximum.

After reaching the out-of-pocket maximum, your insurance pays 100% of covered medical costs for the rest of the plan year.

This gives you financial protection in case of a serious illness, surgery, or accident.

Conclusion: Why Your Health Insurance Deductible Matters

Your health insurance deductible is a key factor in determining how much you’ll spend on medical care. It affects when your insurance begins covering costs and how much you’ll need to pay before that happens.

At AHiX Marketplace, we make it easy to find a health plan that fits your needs and budget. You can compare plans based on deductibles, monthly premiums, out-of-pocket maximums, coverage details, and eligibility for savings or subsidies.

Whether you’re looking for individual coverage, a family plan, or short-term insurance, we provide the information and support you need to make the right choice—so you get the best coverage at the best price.

FAQs:

1. What is health insurance, and why do I need it?

Health insurance is a policy that helps cover medical expenses, including doctor visits, hospital stays, and prescription drugs. It protects you from high healthcare costs and ensures access to necessary medical care.

2. What is the difference between a deductible, copay, and coinsurance?

- Deductible: The amount you pay before insurance starts covering expenses.

- Copay: A fixed amount you pay for specific services, like doctor visits or prescriptions.

- Coinsurance: The percentage of costs you share with your insurer after meeting your deductible.

3. What does out-of-pocket maximum mean?

The out-of-pocket maximum is the highest amount you will pay for covered services in a year. Once you reach this limit, your insurance covers 100% of eligible costs.

4. What is the difference between an HMO, PPO, EPO, and POS plan?

- HMO (Health Maintenance Organization): Requires you to choose a primary care physician (PCP) and get referrals for specialists. Usually lower costs.

- PPO (Preferred Provider Organization): Allows you to see specialists without referrals and visit out-of-network doctors. Higher costs but more flexibility.

- EPO (Exclusive Provider Organization): Covers only in-network care, but no referrals needed for specialists.

- POS (Point of Service): Hybrid of HMO and PPO, requiring referrals but offering some out-of-network coverage.

Note: Some plans may vary. For example, certain carriers in specific states may not require referrals even if the network type usually does. Always check your plan details to be sure.

5. Can I get health insurance if I am unemployed?

Yes, unemployed individuals can apply for ACA marketplace plans, Medicaid (if eligible), or short-term health insurance. Subsidies may help lower costs.

6. What happens if I miss the Open Enrollment deadline?

If you miss Open Enrollment, you can still get coverage if you qualify for a Special Enrollment Period or explore short-term health insurance options.

7. Is a lower or higher deductible better?

- A low deductible plan is better if you expect frequent medical expenses, as insurance starts covering costs sooner.

- A high deductible plan is better if you are healthy and rarely visit the doctor, as it comes with lower monthly premiums.

8. How does my deductible affect my monthly premium?

Plans with higher deductibles usually have lower monthly premiums, while plans with lower deductibles have higher monthly costs. AHiX can help you compare these trade-offs.

9. Can I switch health insurance plans after meeting my deductible?

If you switch plans, your deductible does not carry over. It resets with the new plan, even if you switch mid-year.

10. Where can I find health insurance plans with the best deductibles?

If you’re looking for health insurance plans with deductibles that fit your budget and medical needs, AHiX Marketplace is the best place to start. Our platform allows you to:

- Compare health plans based on deductibles, premiums, and coverage.

- Find low-deductible plans for frequent medical visits or high-deductible plans for lower monthly costs.

- Check if you qualify for subsidies or cost-sharing reductions to lower your deductible.

Explore your options today at AHiX Marketplace and find the best deductible for your situation.