The Individual Coverage Health Reimbursement Arrangement (ICHRA) has become one of the most flexible ways for employers to offer health benefits. Instead of paying for one group health insurance plan, companies can give employees a set monthly allowance to buy their own coverage. This gives employees more choice and helps businesses manage costs.

But with this flexibility comes an important rule: affordability. The Internal Revenue Service (IRS) sets clear guidelines for what constitutes affordable health coverage. If an ICHRA is not affordable, the employer may face penalties, and employees may miss out on the right type of coverage or government subsidies.

Affordability is not just about making plans cheaper, it is about meeting federal compliance rules that keep both employers and workers protected. Understanding how affordability is calculated helps businesses design fair benefit programs and ensures employees can use their ICHRA allowance without financial strain.

In this blog, we will explain how ICHRA affordability is measured, the different calculation methods, real-world examples, and why compliance matters for every employer.

When we talk about affordability in ICHRA, we are looking at how much of an employee’s income goes toward the cost of their health insurance after applying the employer’s reimbursement.

The IRS says that health coverage is considered affordable if the employee’s share of the premium does not go above a certain percentage of their income. In other words, if an employee has to pay too much out of their own pocket, the plan is not affordable.

For ICHRA, the rule is simple:

An employer sets an allowance.

The employee uses that allowance to buy a health plan on the marketplace.

If the remaining premium cost (after the allowance) is within the affordability limit, the plan is affordable.

Why does this matter?

If the ICHRA is affordable, the employee cannot get premium tax credits on the marketplace.

If the ICHRA is not affordable, the employee may decline the ICHRA and apply for government subsidies instead. The employee should check eligibility for subsidies before declining the ICHRA.

This balance makes affordability a key factor for both compliance and employee satisfaction. Employers must design allowances carefully so their workforce has access to affordable coverage that meets legal standards.

Understanding the ICHRA Affordability Percentage

Each year, the IRS sets an affordability percentage to determine whether health coverage is affordable. This percentage is applied to an employee’s household income. If the employee’s share of the premium (after the employer’s ICHRA contribution) is less than this percentage, the coverage is affordable.

For 2026, the affordability percentage is

This number is very important because:

It changes every year, based on IRS rules and inflation.

Employers must use the updated percentage when they set ICHRA allowances.

Using the wrong figure can cause a business to fail the affordability test and risk non-compliance.

The affordability percentage acts like a guardrail. It ensures employees are not burdened with coverage costs that take up too much of their income and keeps employer health benefit programs within federal standards.

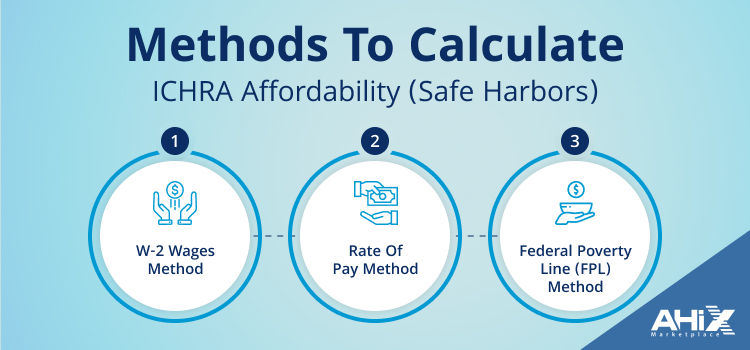

Methods to Calculate ICHRA Affordability (Safe Harbors)

Employers may not always know an employee’s exact household income, which makes it difficult to test affordability. To solve this, the IRS allows the use of safe harbors simplified methods that employers can use instead of tracking each worker’s total income.

There are three main safe harbor methods:

1. W-2 Wages Method

This method uses an employee’s wages reported in Box 1 of their W-2 form as the income base.

How it works:

Take the employee’s annual W-2 wages.

Multiply by the IRS affordability percentage (9.96% for 2026).

Compare the employee’s required premium contribution (after the ICHRA allowance) to this number.

Example:

Employee earns $36,000 (W-2 wages).

9.96% × $36,000 = $3,586.

As long as the employee’s share of the premium is less than $3,586/year (≈ $299/month), the ICHRA is affordable.

Pros: Uses actual income data, precise for each employee. Cons: Employers won’t know if they passed the test until year-end, making in-year adjustments harder.

2. Rate of Pay Method

This method uses the employee’s hourly rate or monthly salary to estimate income.

How it works:

For hourly employees: hourly rate × 130 hours/month.

For salaried employees: use the monthly salary.

Multiply that number by 9.96% to find the maximum affordable premium.

Example (Hourly Worker):

Hourly rate = $15/hour.

$15 × 130 = $1,950/month income.

9.96% × $1,950 = $194/month maximum affordable premium.

If the employee’s share after ICHRA allowance is $190/month, coverage is affordable.

Pros: Easy to calculate, doesn’t rely on household income. Cons: May not reflect actual earnings if hours fluctuate.

3. Federal Poverty Line (FPL) Method

This method uses the Federal Poverty Line (FPL) as a simple baseline.

How it works:

Use the 2026 FPL for a single individual, even if the employee has dependents.

Multiply the monthly FPL figure by 9.96% to determine the maximum affordable premium.

Example:

2026 FPL for a single person ≈ $1,310/month.

9.96% × $1,310 = $130/month maximum affordable premium.

If the employee’s share after ICHRA allowance is $125/month, coverage is affordable.

Pros: Very clear, protects lower-income employees, safest for compliance. Cons: Often requires higher employer allowances, increasing costs.

Summary of Safe Harbors (2026)

Method

Key Feature

Pros

Cons

W-2 Method

Uses actual annual wages

Accurate per employee

Results known after year-end

Rate of Pay Method

Uses hourly or monthly pay rate

Simple and predictable

May not reflect variable hours

FPL Method

Based on federal poverty guidelines

Easiest and safest for compliance

Usually costs employers more

By choosing the right safe harbor method, employers can make sure their ICHRA program meets affordability rules while balancing business costs.

Why Affordability Matters for Compliance

Affordability is not only about making coverage fair for employees, it is also a legal requirement under the Affordable Care Act (ACA). Employers who offer ICHRA must make sure their plan is affordable, or they could face serious compliance problems.

Here’s why it matters:

1. Employer Mandate Penalties

Large employers (with 50 or more full-time workers) are required by the ACA to provide affordable health coverage. If their ICHRA is unaffordable, they may face tax penalties. These fines can add up quickly and create unnecessary financial risk for the business.

2. Employee Subsidies

If an ICHRA is unaffordable, employees can decline it and apply for premium tax credits on the Health Insurance Marketplace. This can lead to confusion for workers, especially if they are not sure whether the ICHRA or the subsidy gives them better value.

3. IRS Compliance

Affordability tests are not optional. Employers must use one of the safe harbor methods to prove they meet the rule. Failing to keep proper documentation or miscalculating allowances could trigger compliance issues during an IRS review.

4. Employee Trust and Retention

Beyond legal rules, affordability impacts how employees view their benefits. If workers feel their ICHRA allowance does not make coverage affordable, they may see it as unfair, which can hurt morale and retention.

In short, affordability matters because it protects both employers and employees. It ensures compliance with federal law, helps avoid costly penalties, and builds trust by showing that the employer is serious about offering real, usable health benefits.

Real-Life Scenarios of ICHRA Affordability

Understanding affordability rules becomes much clearer when we look at real examples. Here are three scenarios showing how affordability is tested in different situations:

Scenario 1: Full-Time Salaried Worker

Maria earns $50,000 per year.

Her employer offers an ICHRA allowance of $400 per month.

The lowest-cost silver plan in her area costs $600 per month.

Using the rate of pay method: $16 × 130 hours = $2,080/month.

Affordability test: 8.39% × $2,080 = $174/month.

His health plan costs $350/month, and the employer gives $200 allowance.

James’s share = $150/month.

Since $150 < $174, coverage is affordable under the rate of pay method.

Scenario 3: Low-Income Employee

Sarah earns $18,000 per year.

Employers contribute $250/month toward ICHRA.

Marketplace plan costs $350/month.

Sarah’s share = $100/month.

Using the Federal Poverty Line method (FPL ~ $1,255/month): 8.39% × $1,255 = $105/month. Since $100 < $105, coverage is affordable.

Why These Scenarios Matter

They show that affordability depends on both income and employer allowance.

The same allowance may be affordable for one employee but not another.

Employers must carefully choose which safe harbor method to use so the ICHRA program works for their entire workforce.

Strategies to Keep Your ICHRA Affordable

Offering an ICHRA is not just about giving employees money for health coverage. It’s about making sure the allowance is designed in a way that meets affordability rules. Here are some strategies employers can use:

1.Review Workforce Income Levels

Every workplace is different. A fixed allowance may be affordable for higher earners but not for lower earners. Employers should study their employee pay structure before deciding how much to contribute.

2. Choose the Right Safe Harbor Method

If most employees have steady salaries, the W-2 method works well.

If many are hourly workers, the Rate of Pay method may be easier.

If the company wants the safest compliance route, the FPL method offers the most protection.

3. Adjust Allowances by Employee Class

ICHRA rules allow employers to group workers into classes (like full-time, part-time, seasonal, or salaried). Each class can receive a different allowance. This flexibility helps ensure affordability across diverse employee groups.

1. Plan for Annual Updates

Since the affordability percentage changes every year, employers must revisit their allowances annually. What was affordable this year may not be next year if the percentage drops.

2.Use Affordability Tools

Employers can use affordability calculators or work with licensed advisors to test their planned contributions before rolling them out. This reduces the chance of surprises later.

By following these strategies, employers can design ICHRA allowances that not only comply with IRS rules but also give employees real value and peace of mind.

Common Mistakes Employers Make With Affordability

Even with clear IRS rules, many employers make small errors that can cause their ICHRA to fail the affordability test. Here are some of the most common mistakes to avoid:

1. Not Updating for the New Year

The affordability percentage changes every year. Some employers forget to adjust their ICHRA contributions when the IRS lowers the percentage, which can suddenly make coverage unaffordable.

2. Applying the Wrong Safe Harbor Method

Employers may choose a method that doesn’t match their workforce. For example, using the W-2 method for hourly workers with unpredictable income can give misleading results.

3. One-Size-Fits-All Allowances

Giving the same allowance to all employees without considering different income levels or job classes often leads to unfair or unaffordable results for lower-paid workers.

4. Failing to Document Calculations

Employers sometimes don’t keep written records of how they tested affordability. If audited by the IRS, lack of proof can create compliance problems even if the plan was actually affordable.

5. Ignoring Part-Time or Seasonal Employees

These workers are often overlooked when allowances are set. But if they are offered an ICHRA, their affordability must still be checked using safe harbor rules.

6. Assuming Marketplace Prices Stay the Same

Premiums for health plans vary by region and change each year. Relying on outdated cost estimates can lead to miscalculations.

By avoiding these mistakes, employers can design ICHRA benefits that stay compliant and genuinely affordable for their workforce.

FAQs:

1. How does the IRS define ICHRA affordability?

The IRS defines affordability by comparing the employee’s required premium contribution (after ICHRA allowance) to a set percentage of income (8.39% for 2025).

2. Is ICHRA affordability based on household income or just wages?

Affordability is technically measured against household income, but employers can use safe harbor methods (W-2, Rate of Pay, or FPL) as alternatives since they may not know household details.

3. Can ICHRA allowances vary for different employee groups?

Yes. Employers can set different allowance amounts for classes like full-time, part-time, or seasonal workers. This helps tailor affordability across the workforce.

4. Does ICHRA affordability affect an employee’s ability to get marketplace subsidies?

Yes. If an ICHRA is affordable, employees cannot claim subsidies. If it is unaffordable, they may decline the ICHRA and qualify for premium tax credits.

5. What role does the lowest-cost silver plan play in affordability?

The affordability test is based on the premium for the lowest-cost silver plan available in the employee’s area, not the plan the employee chooses.

6. Do dependents count when testing ICHRA affordability?

No. Affordability is measured only for self-only coverage, not family or dependent coverage. Employers only need to check if the allowance makes single coverage affordable.

7. How often must employers check affordability for ICHRA?

Employers must test affordability each plan year and adjust contributions whenever the IRS updates the affordability percentage.

8. What happens if an employer miscalculates ICHRA affordability?

If the plan fails affordability, employees may be eligible for subsidies, and the employer could face ACA employer mandate penalties.

9. Is there a safe harbor method better suited for small businesses?

Yes. The Federal Poverty Line (FPL) safe harbor is often used by smaller businesses because it provides the clearest compliance protection.

10. Can employers use different safe harbor methods for different employees?

No. An employer must apply the same safe harbor method consistently across a given class of employees, but they may use different methods for different classes.