The 2026 HSA contribution limit is $4,400 for self-only coverage and $8,750 for family coverage. If you are age 55 or older, you can contribute an extra $1,000 catch-up amount. For 2026, all Bronze and Catastrophic Marketplace plans are also HSA-eligible under the new law.

The IRS released the 2026 Health Savings Account (HSA) contribution limits in IRS Revenue Procedure 2025-19 (May 1, 2025). Individual limits rise to $4,400 and family limits to $8,750. But the bigger story for 2026 is the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, which is the most significant expansion of HSA eligibility since these accounts were created in 2003.

IRS Notice 2026-5 (December 9, 2025) provides the official technical guidance. It permanently extends telehealth pre-deductible coverage, makes Bronze and Catastrophic ACA Exchange plans HSA-compatible, and allows Direct Primary Care Service Arrangements (DPCSAs) as HSA-eligible expenses, effective January 1, 2026.

2026 HSA Quick Answer

- Self-only contribution limit: $4,400

- Family contribution limit: $8,750

- Catch-up age 55+: $1,000

- HDHP min deductible: $1,700 self / $3,400 family

- HDHP max OOP: $8,500 self / $17,000 family

- New in 2026: Bronze and Catastrophic Marketplace plans are HSA-eligible

This guide covers all of these changes in full, along with how 2026 HDHP requirements compare to ACA out-of-pocket limits, a complete FAQ section updated for the new rules, and clear guidance on whether an HSA-qualified plan is right for your situation.

1. What Are the 2026 HSA Contribution Limits?

For calendar year 2026, per IRS Revenue Procedure 2025-19, the HSA contribution limits are as follows. These limits apply to the combined total of your contributions plus any employer contributions.

| Coverage Type | 2024 Limit | 2025 Limit | 2026 Limit |

| Individual (Self-Only) | $4,150 | $4,300 | $4,400 |

| Family Coverage | $8,300 | $8,550 | $8,750 |

| Catch-up (Age 55+) | $1,000 | $1,000 | $1,000 |

Source: IRS Revenue Procedure 2025-19 (May 1, 2025) | IRS Publication 969

What counts toward the limit: Every dollar contributed to your HSA whether by you, your employer, or a family member counts toward the annual limit. If your employer contributes $1,200 to your self-only HSA, you may personally contribute only $3,200 more to reach the $4,400 cap.

The catch-up contribution: If you are 55 or older at the end of the tax year and not enrolled in Medicare, you may contribute an additional $1,000 on top of the standard limit ($5,400 for self-only, $9,750 for family in 2026). If both spouses are 55 or older, each must maintain a separate HSA to claim their own catch-up contribution.

The last-month rule: If you are HSA-eligible on December 1, 2026, you may contribute the full annual limit even if you were not eligible for the entire year. However, you must remain enrolled in an HSA-qualified plan through December 31, 2027 (the testing period). If you fail this test for reasons other than death or disability, excess contributions become taxable income plus a 10% penalty.

Deadline: You may contribute to your 2026 HSA at any time up to April 15, 2027.

2.2026 HDHP Requirements: What Makes a Plan HSA-Eligible?

To contribute to an HSA, you must be enrolled in a qualifying High Deductible Health Plan (HDHP). For 2026, IRS Rev. Proc. 2025-19 sets the following thresholds:

| HDHP Requirement | 2025 | 2026 | Change |

| Min. Deductible (Self-Only) | $1,650 | $1,700 | +$50 |

| Min. Deductible (Family) | $3,300 | $3,400 | +$100 |

| OOP Max (Self-Only) | $8,300 | $8,500 | +$200 |

| OOP Max (Family) | $16,600 | $17,000 | +$400 |

| Embedded Deductible Floor | $3,300 | $3,400 | +$100 |

Source: IRS Revenue Procedure 2025-19 (May 1, 2025)

What counts toward the out-of-pocket maximum?

The HDHP out-of-pocket maximum includes in-network deductibles, copayments, and coinsurance but does not include insurance premiums. Costs for out-of-network services generally do not count toward the in-network maximum.

Embedded deductibles in family plans

A family HDHP may set a per-person (embedded) deductible, but that embedded deductible cannot be lower than the $3,400 family minimum. If any individual’s deductible within a family plan falls below $3,400, the plan loses HDHP status, and members lose HSA contribution eligibility. This is a critical compliance point for employers offering family HDHPs.

Updated rule: Telehealth is no longer disqualifying (effective Jan. 1, 2025)

3.OBBBA 2026: The Biggest Expansion of HSA Access Since 2003

The One Big Beautiful Bill Act (OBBBA), Pub. L. 119-21, was signed July 4, 2025. It amended Section 223 of the Internal Revenue Code in three ways that materially change who qualifies for an HSA in 2026 and beyond. IRS Notice 2026-5 (December 9, 2025) provides the official technical guidance for all three changes.

If you want a deeper breakdown of how these law changes affect ACA plans and eligibility, read our full guide on HSA changes under the Big Beautiful Bill and ACA Bronze plan eligibility.

Three OBBBA changes that took effect January 1, 2026:

- Bronze and Catastrophic ACA plans are now HSA-compatible. 2. Telehealth pre-deductible coverage is permanently allowed (retroactive to January 1, 2025). 3. Direct Primary Care Service Arrangements (DPCSAs) no longer disqualify HSA eligibility.

Change 1: Bronze and Catastrophic Plans Are Now HSA-Compatible (Effective Jan. 1, 2026)

Before the OBBBA, Bronze and Catastrophic plans sold on ACA Exchanges could not qualify as HDHPs because their deductible and out-of-pocket structures fell outside the statutory HDHP band. Millions of Americans enrolled in these plans were therefore ineligible for an HSA despite having high out-of-pocket exposure.

Section 71307 of the OBBBA amends Section 223(c)(2) of the Internal Revenue Code to automatically treat any Bronze or Catastrophic plan available as individual coverage through an ACA Exchange as an HSA-compatible HDHP, even if it does not meet the standard deductible minimums or OOP maximums.

What this means for you:

- If you are enrolled in a Bronze or Catastrophic ACA Exchange plan as of January 1, 2026, you may open and contribute to an HSA.

- The standard HDHP minimum deductible ($1,700/$3,400) and OOP maximum ($8,500/$17,000) requirements are waived for these plans.

- Off-exchange Bronze or Catastrophic plans also qualify if the same plan is available as individual coverage through an Exchange, or if the individual reasonably believes it is.

- Employer-sponsored Individual Coverage HRAs (ICHRAs) or Qualified Small Employer HRAs (QSEHRAs) may be used to purchase Bronze or Catastrophic coverage without affecting HSA-eligible HDHP status.

- Note: This provision applies to individual coverage only. It does not extend to Small Business Health Options Program (SHOP) or other small/medium employer group exchange purchases.

Source: OBBBA Section 71307; IRS Notice 2026-5, Q&As 4-7

Change 2: Telehealth Pre-Deductible Coverage Is Now Permanent (Retroactive to Jan. 1, 2025)

Section 71306 of the OBBBA permanently codifies the telehealth safe harbor that Congress twice extended on a temporary basis under the CARES Act and subsequent legislation. The rule is effective retroactively for plan years beginning on or after January 1, 2025.

What this means for you:

- An HDHP may cover telehealth and remote care services before the minimum deductible is met without disqualifying members from HSA contributions.

- There is no longer any need for annual Congressional renewal of this safe harbor.

- The IRS identifies eligible telehealth services by reference to the CMS annual list of Medicare-reimbursable telehealth services (published under Section 1834(m)(4)(F) of the Social Security Act).

- In-person services, medical equipment, or drugs provided in connection with a telehealth visit are NOT covered by this safe harbor and remain subject to the normal deductible rules, unless those items independently qualify as telehealth services under applicable guidance.

- Importantly, if your HDHP covered telehealth pre-deductible before the OBBBA was enacted on July 4, 2025, IRS Notice 2026-5 confirms you remain eligible to contribute to your HSA for all of 2025, provided your plan otherwise met HDHP requirements.

Source: OBBBA Section 71306; IRS Notice 2026-5, Q&As 1-3

Change 3: Direct Primary Care Service Arrangements (DPCSAs) Are Now HSA-Compatible (Effective Jan. 1, 2026)

Before the OBBBA, the IRS treated enrollment in a Direct Primary Care arrangement as ‘other coverage’ that disqualified individuals from HSA contributions. Section 71308 of the OBBBA removes this disqualification and allows HSA funds to pay DPCSA fees as qualified medical expenses.

How a DPCSA qualifies under IRS Notice 2026-5:

- The arrangement must provide only primary care services from primary care practitioners.

- The sole compensation must be a fixed periodic fee (no per-service charges).

- The arrangement must not include procedures requiring general anesthesia, prescription drugs (other than vaccines), or laboratory services not typically administered in an ambulatory primary care setting.

- Monthly fees must not exceed $150 for individuals or $300 for families to maintain HSA contribution eligibility. These limits will be adjusted annually for inflation after 2026.

- Fees above the monthly threshold may still be reimbursed from an existing HSA balance, but doing so will disqualify the individual from making new HSA contributions during that period.

- If your employer pays your DPCSA fees — including through a Section 125 cafeteria plan salary reduction — those fees cannot be reimbursed from your HSA.

Source: OBBBA Section 71308; IRS Notice 2026-5, Q&As 8-16

4. How 2026 HSA HDHP Limits Compare to ACA Out-of-Pocket Limits

One of the most important distinctions for anyone shopping health insurance in 2026 is that the HSA HDHP out-of-pocket maximums are set independently from — and are more restrictive than — the ACA’s overall out-of-pocket maximums. Here is how they compare for 2026:

| Limit Type | Self-Only 2026 | Family 2026 |

| ACA Out-of-Pocket Maximum (all plans) | $10,600 | $21,200 |

| HDHP Out-of-Pocket Maximum (HSA-eligible health plan) | $8,500 | $17,000 |

| Difference (HDHP more protective) | -$2,100 | -$4,200 |

Source: IRS Rev. Proc. 2025-19 (High Deductible Health Plans limits); HHS Notice of Benefit and Payment Parameters for 2026 (ACA limits)

Why does this difference matter?

For the 2026 plan year, a Marketplace plan cannot have an out-of-pocket limit above $10,600 for an individual or $21,200 for a family. By contrast, a standard HSA-qualified HDHP must keep out-of-pocket limits at or below $8,500 for self-only coverage and $17,000 for family coverage. That means standard HSA-qualified HDHPs remain more restrictive than the general ACA cost-sharing ceiling.

As of 2026, Bronze and Catastrophic Marketplace plans are treated as HSA-compatible even if they do not fall within the usual HDHP deductible or out-of-pocket thresholds. So some HSA-compatible Bronze or Catastrophic plans may have out-of-pocket limits above the standard HDHP ceiling, which is now allowed under the new law.

Since the OBBBA, Bronze and Catastrophic plans are now treated as HSA-compatible regardless of whether they meet the HDHP OOP thresholds. This means some Bronze plans will have OOP maximums above the HDHP standard — which is now expressly permitted for these plan types under Section 71307.

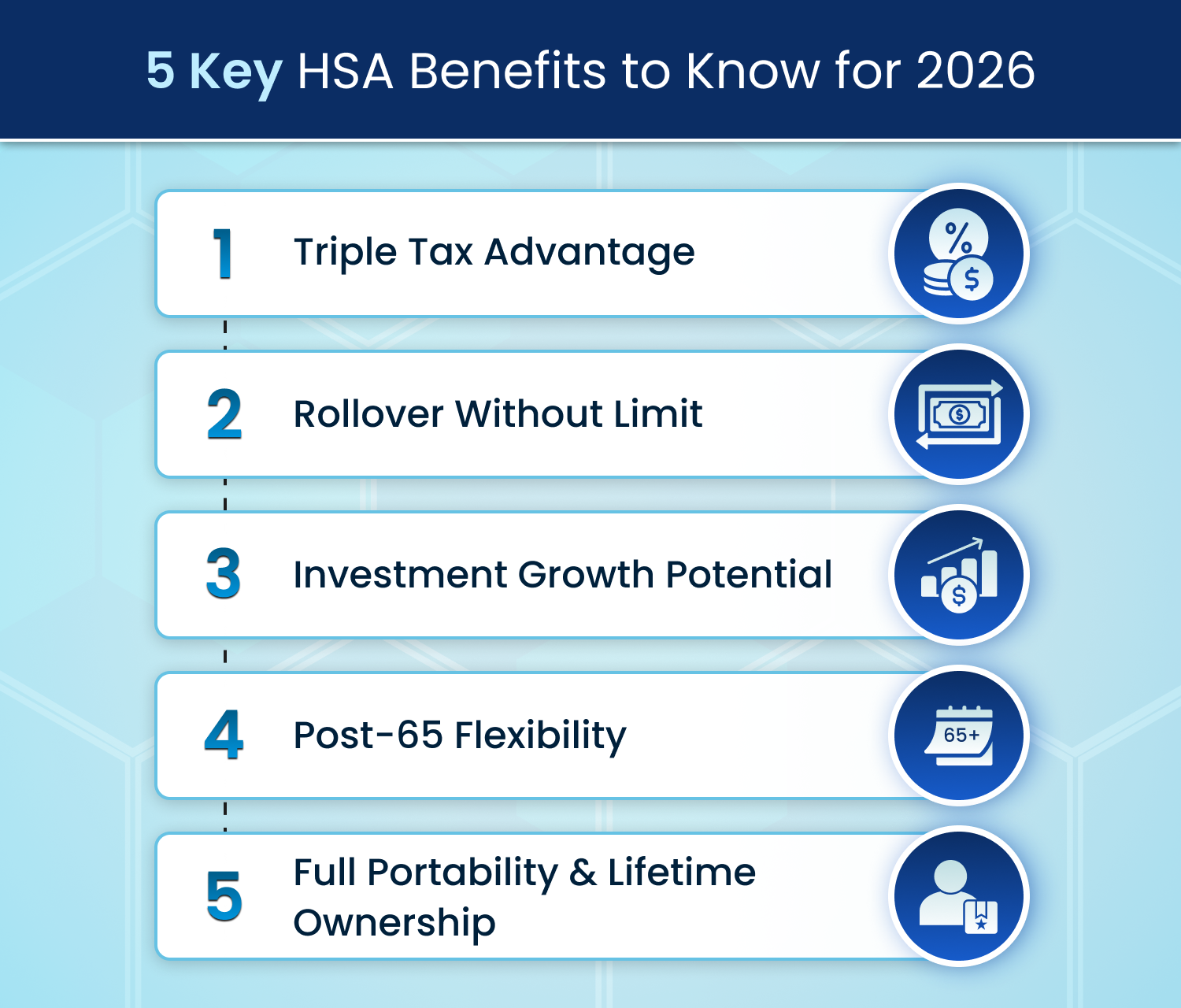

5. Five Core HSA Benefits Worth Understanding for 2026

1. Triple Tax Advantage

An HSA is one of the only financial accounts in the U.S. tax code that provides tax benefits at three points: contributions reduce your taxable income (or are pre-tax via payroll), growth through interest and investment gains is tax-free, and withdrawals for qualified medical expenses are also tax-free. No other widely available savings vehicle not a 401(k), not a Roth IRA provides all three.

2.Rollover Without Limit

Unlike a Flexible Spending Account (FSA), which imposes a use-it-or-lose-it rule (with only a small rollover option), your HSA balance rolls over in full every year and never expires. Because HSA balances can be invested and roll over indefinitely, they may become a meaningful long-term healthcare savings tool over time, especially for people who contribute consistently and leave funds invested for many years.

3.Investment Growth Potential

Most HSA providers allow you to invest your balance in mutual funds, ETFs, or other instruments once you reach a threshold (commonly $1,000 to $2,000). The invested gains grow tax-free. This makes an HSA a powerful long-term savings vehicle, not merely a spending account.

4. Post-65 Flexibility

After age 65, an HSA functions like a traditional IRA for non-medical withdrawals: you pay ordinary income tax but no penalty. For qualified medical expenses, withdrawals remain tax-free in retirement, which is one reason HSAs are often used as a long-term healthcare savings tool. There are no required minimum distributions (RMDs) from an HSA, unlike a traditional IRA.

5. Full Portability and Lifetime Ownership

Your HSA belongs to you, not your employer. If you change jobs, retire, or switch insurance plans, the balance travels with you. You may continue spending from an existing HSA even after you lose HDHP eligibility — you simply cannot make new contributions during that period.

6.Is an HSA-Qualified Plan the Right Choice for You in 2026?

For designer generate banner image with text Understanding HSA-Qualified Plans for 2026

The decision to enroll in an HSA-qualified HDHP is a function of your expected healthcare utilization, financial position, and risk tolerance. It is not universally correct for everyone.

People likely to benefit from an HSA-qualified plan

- Generally healthy individuals who rarely use medical services beyond preventive care

- Those who can afford to self-fund the deductible from emergency savings or HSA contributions

- High earners who benefit most from the tax deduction on contributions

- Those who want to build a tax-advantaged healthcare reserve for retirement

- As of January 1, 2026: Bronze or Catastrophic ACA plan enrollees who want to start an HSA for the first time

- Individuals enrolled in Direct Primary Care arrangements who want to use HSA funds tax-free for DPC fees

People who may be better served by a lower-deductible plan

- Those with chronic conditions requiring frequent specialist visits, prescriptions, or procedures

- Families with children who have predictably high healthcare utilization

- Individuals who cannot afford to hold the full deductible in liquid savings

- Anyone currently enrolled in Medicare (who cannot contribute to an HSA regardless)

Factors to evaluate

- Compare the premium savings of an HDHP vs. a PPO/HMO over 12 months

- Model your expected out-of-pocket costs under both plan types

- Determine whether your employer contributes to HSAs — employer contributions reduce your personal funding requirement

- Consider whether you will use your HSA as a spending account (short-term) or an investment vehicle (long-term)

You can compare HSA-compatible and non-HSA ACA plans side by side on the AHiX Marketplace to model the cost difference for your specific situation.

7. Frequently Asked Questions: 2026 HSA Rules (Including OBBBA)

Q1. Can I open an HSA if I have a Bronze or Catastrophic ACA plan in 2026?

Yes. The OBBBA, effective January 1, 2026, reclassified Bronze and Catastrophic ACA Exchange plans as HSA-compatible HDHPs. You may contribute up to $4,400 (self-only) or $8,750 (family) to an HSA in 2026 if you are enrolled in one of these plans, provided you have no other disqualifying coverage. This applies even if your plan does not meet the standard HDHP minimum deductible or OOP maximum thresholds. Source: OBBBA Section 71307; IRS Notice 2026-5.

Q2. Does telehealth coverage affect my HSA eligibility in 2026?

No. As of plan years beginning January 1, 2025, HDHPs may cover telehealth and remote care services before the minimum deductible is met without disqualifying members from HSA contributions. This rule was made permanent by the OBBBA. It is retroactive to January 1, 2025 — meaning if your plan covered telehealth pre-deductible before July 4, 2025 (when the OBBBA was signed), your 2025 HSA contributions remain valid. Source: OBBBA Section 71306; IRS Notice 2026-5.

Q3. What is a Direct Primary Care arrangement and how does it affect my HSA in 2026?

A Direct Primary Care Service Arrangement (DPCSA) is a healthcare model in which you pay a fixed monthly fee directly to a primary care physician for a comprehensive package of services. Before 2026, enrollment in a DPC arrangement was treated as disqualifying coverage, preventing you from contributing to an HSA. The OBBBA removed this restriction effective January 1, 2026. You may now contribute to an HSA and remain enrolled in a DPCSA, provided the monthly fee does not exceed $150 (individual) or $300 (family). You may also use HSA funds to pay these fees as qualified medical expenses. Source: OBBBA Section 71308; IRS Notice 2026-5.

Q4. What are the official IRS sources for the 2026 HSA limits?

The contribution limits and HDHP thresholds are set by IRS Revenue Procedure 2025-19 (May 1, 2025). The OBBBA eligibility expansion is governed by IRS Notice 2026-5 (December 9, 2025), which is available directly from the IRS at irs.gov/pub/irs-drop/n-26-05.pdf. Additional reference: IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans.

Q5. What happens if I exceed the 2026 HSA contribution limit?

Contributions above the annual limit are subject to a 6% excise tax per year for every year the excess remains in the account. To avoid the penalty, you must withdraw the excess contribution plus any earnings attributable to it before the tax filing deadline — typically April 15, 2027, for the 2026 tax year. The withdrawn amount is includable in your gross income.

Q6. Does my employer’s contribution count toward my 2026 HSA limit?

Yes. All contributions to your HSA from any source count toward the annual limit ($4,400 for self-only, $8,750 for family in 2026). If your employer contributes $1,500 to your self-only HSA, the maximum you may personally add is $2,900.

Q7. Can I contribute to an HSA if I switch health plans mid-year in 2026?

Your maximum contribution is prorated based on the number of months you were enrolled in an HSA-qualified plan. Under the last-month rule, if you are enrolled as of December 1, 2026, you may contribute the full annual limit — but you must remain enrolled in an HSA-qualified plan through December 31, 2027 (the testing period) or face income tax and a 10% penalty on the excess.

Q8. Can both spouses contribute to separate HSAs in 2026?

Yes, but the combined total of both accounts cannot exceed the family limit ($8,750 in 2026). If both spouses are age 55 or older, each may make their own $1,000 catch-up contribution to their separate accounts, for a combined maximum of $10,750.

Q9. Can I use HSA funds for dental, vision, and over-the-counter expenses?

Yes to all three. Qualified HSA expenses include dental procedures and exams, vision care and prescription eyewear, and over-the-counter medications and menstrual care products (the latter two without a prescription, per the CARES Act which remains in effect in 2026). Full lists are available in IRS Publication 502.

Q10. Can I contribute to an HSA and still qualify for ACA premium tax credits?

Possibly, yes. HSA eligibility and premium tax credit eligibility are separate rules. You may still qualify for ACA premium tax credits if your income and household circumstances meet Marketplace requirements and you enroll in a plan that is HSA-eligible.

However, be careful with tax wording: deductible HSA contributions can reduce adjusted gross income, and Marketplace subsidy calculations are based on modified adjusted gross income (MAGI), which starts with AGI. That means HSA contributions may affect the amount of premium tax credit you qualify for. The impact depends on your income, filing status, and how the contribution is made.

For tax-credit calculations, it is safest to estimate both your expected Marketplace MAGI and your planned HSA deductions before enrolling.

Q11. Can I keep and spend from my HSA if I switch to a non-HDHP plan?

Yes. Your existing HSA balance is yours permanently. You may continue to withdraw funds for qualified medical expenses tax-free even after you lose HDHP eligibility. You simply cannot make new contributions to the account until you return to an HSA-qualifying plan.

Q12. What is the penalty for using HSA funds for non-medical expenses?

Before age 65: withdrawals for non-qualified expenses are included in gross income and subject to a 20% penalty. After age 65: withdrawals for non-qualified expenses are included in gross income but no penalty applies — the same tax treatment as a traditional IRA.

Q13. Does a family HDHP with a $2,500 per-person embedded deductible qualify in 2026?

No. The embedded individual deductible within a family HDHP cannot be lower than the family minimum deductible ($3,400 in 2026). A $2,500 per-person embedded deductible renders the plan non-compliant, and members cannot make HSA contributions during the period of enrollment.

Q14. When must I contribute to receive the HSA deduction for the 2026 tax year?

You may contribute to your 2026 HSA at any point from January 1, 2026 through April 15, 2027. You do not have to make contributions within the calendar year — contributions made between January 1 and April 15, 2027 can be designated as 2026 contributions.

Q15. Can I invest my HSA balance in 2026?

Yes. Once your balance exceeds the investment threshold set by your HSA provider (typically $1,000 to $2,000), you may invest in mutual funds, ETFs, or other instruments. Investment earnings grow tax-free if you use them for qualified medical expenses. Check your provider’s specific options and fees.