Choosing a health insurance plan can feel confusing when every option uses short names like PPO, HMO, EPO, POS, Bronze, Silver, Gold, deductible, copay, coinsurance, and out-of-pocket maximum.

One of the most common plan types people search for is a PPO plan.

A PPO plan, also called a Preferred Provider Organization plan, is a type of health insurance plan that gives you more flexibility when choosing doctors, hospitals, and specialists. You usually pay less when you use doctors in the plan’s network, but you may still have some coverage if you go outside the network. HealthCare.gov defines a PPO as a plan where you pay less for in-network providers but can use out-of-network doctors and hospitals without a referral for an added cost.

That flexibility is the main reason many people like PPO plans. But PPO plans can also come with higher monthly premiums, higher deductibles, or more cost-sharing than more restrictive network plans, depending on the insurer, state, metal level, and benefits. Some insurers describe PPOs as flexible plans that may cost more than HMO or EPO options because they offer broader access and out-of-network benefits.

This guide explains what a PPO plan means, how it works, what it may cost, when it fits, and what to check before enrolling.

Quick Answer: What Is a PPO Plan?

A PPO plan is a health insurance plan that lets you visit doctors, specialists, hospitals, and other providers inside the plan’s preferred network, usually at lower costs. It may also let you use out-of-network providers, but you will usually pay more.

In simple words:

| PPO Feature | What It Means |

| Full name | Preferred Provider Organization |

| Primary care doctor required? | Usually no |

| Specialist referral required? | Usually no |

| In-network care | Usually costs less |

| Out-of-network care | Usually allowed, but costs more |

| Best for | People who want provider flexibility |

| Main drawback | May have higher premiums or out-of-pocket costs |

A PPO can be a good choice if you want more control over your doctors and do not want to ask for a referral every time you need a specialist.

What Does PPO Stand For?

PPO stands for Preferred Provider Organization.

The word “preferred” means the insurance company has a network of doctors, hospitals, clinics, specialists, labs, imaging centers, pharmacies, and other healthcare providers that have agreed to work with the plan.

These providers are called in-network providers.

When you use in-network providers, your plan usually pays a larger share of the cost. When you go outside the network, your plan may still help pay, but your share of the bill is usually higher.

This is different from many HMO plans, which usually limit coverage to in-network care except in emergencies and may require you to live or work in the service area. HealthCare.gov explains that HMO plans generally do not cover out-of-network care except emergency care, while PPO plans allow out-of-network care at an added cost.

For a full side-by-side comparison, you can also read AHiX’s existing guide on HMO vs PPO Insurance in 2026.

How Does a PPO Plan Work?

A PPO plan works around two main cost levels:

- In-network care

- Out-of-network care

You are encouraged to use doctors and hospitals inside the PPO network because they usually cost less. But unlike some more restrictive plans, a PPO may still give you coverage when you go outside the network.

Here is a simple example.

Let’s say you need to see a dermatologist.

With many PPO plans, you can:

- Search for an in-network dermatologist.

- Book an appointment directly.

- Visit the specialist without asking your primary care doctor for a referral.

- Pay the in-network specialist copay or coinsurance listed in your plan.

If you choose an out-of-network dermatologist, your PPO may still offer some coverage, but you may pay more. You may also have a separate out-of-network deductible, higher coinsurance, or a risk of balance billing, depending on the provider and plan rules.

That is why PPO flexibility is valuable, but it still requires careful comparison of plans.

PPO Plan Network Rules Explained

The network is one of the most important parts of a PPO plan.

A PPO network is a list of providers that contract with the insurance company. These providers agree to certain rates for covered services. Because of that agreement, your cost is usually lower when you stay in the network.

In-Network PPO Care

In-network care is usually the most affordable way to use a PPO plan.

In-network providers may include:

- Primary care doctors

- Specialists

- Urgent care centers

- Hospitals

- Labs

- Imaging centers

- Pharmacies

- Physical therapists

- Mental health professionals

When you use in-network care, your plan may apply lower copays, lower coinsurance, and better negotiated rates.

Out-of-Network PPO Care

Out-of-network care means you use a provider who does not have a contract with your plan.

A PPO may still cover some out-of-network care, but you should expect higher costs. You may have:

- A higher deductible

- Higher coinsurance

- Higher out-of-pocket responsibility

- More paperwork

- Possible balance billing

- A separate out-of-network out-of-pocket limit, depending on the plan

This is one of the biggest mistakes people make with PPO plans. They hear “out-of-network coverage” and assume the plan will pay most of the bill. That is not always true.

Before using an out-of-network provider, always check:

- Is the provider truly out of network?

- What percentage will the plan pay?

- Does the provider bill the difference?

- Is prior authorization required?

- Is there a separate out-of-network deductible?

- Does the service count toward your out-of-pocket maximum?

If you want to compare plan networks side by side, you can start with the AHiX plan grid.

Do PPO Plans Require Referrals?

Most PPO plans do not require referrals for specialists.

This is one of the main reasons people choose PPO coverage.

For example, if you need to see a cardiologist, orthopedic doctor, dermatologist, allergist, or physical therapist, many PPO plans allow you to make the appointment directly.

That can be helpful if you:

- Already have a specialist

- Manage a chronic condition

- Need faster access to care

- Travel often

- Have children who see different doctors

- Want more control over your healthcare decisions

Still, “no referral” does not always mean “no approval.” Some PPO plans may still require prior authorization for certain services, tests, procedures, surgeries, imaging, or expensive medications.

So, before scheduling costly care, check whether the plan requires approval first.

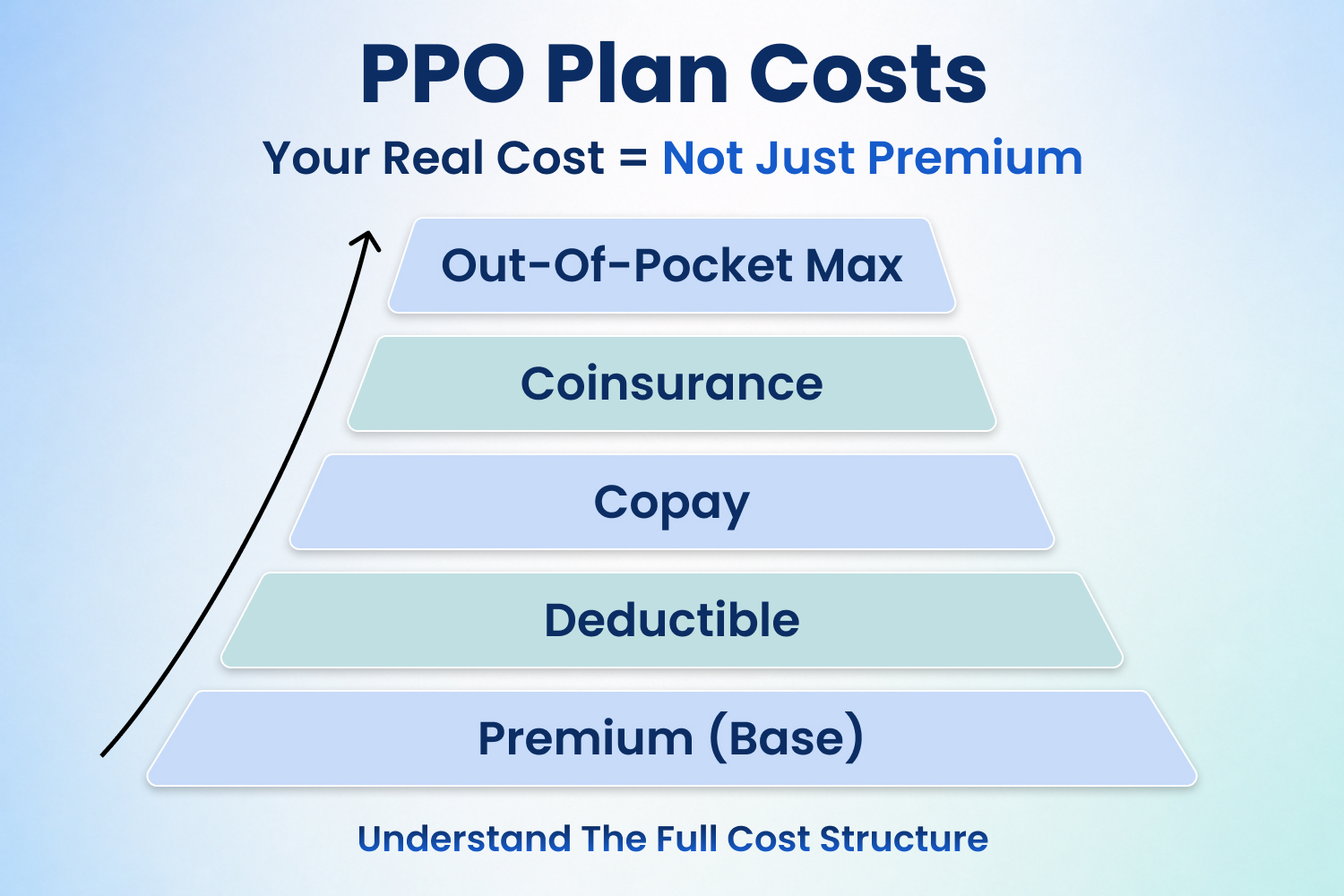

PPO Plan Costs: What Do You Pay?

A PPO plan cost is not just one number. You need to look at the full cost picture.

Your total PPO cost may include:

- Monthly premium

- Deductible

- Copays

- Coinsurance

- Prescription drug costs

- In-network out-of-pocket maximum

- Out-of-network costs

- Non-covered services

HealthCare.gov explains that when comparing plans, people should look at total healthcare costs, not only the monthly premium. Marketplace plans also use metal levels such as Bronze, Silver, Gold, and Platinum to show how you and the plan share costs; these categories do not measure quality of care.

1. Monthly Premium

The premium is the amount you pay every month to keep your plan active.

A PPO plan may have a higher premium than a more restrictive HMO or EPO plan because it usually offers more provider flexibility. But this is not always true in every state or county. Prices depend on your location, age, insurer, metal tier, household size, and subsidy eligibility.

2. Deductible

The deductible is the amount you may need to pay for covered services before the plan starts paying a larger share.

Some PPO plans have separate deductibles for:

- In-network care

- Out-of-network care

This matters a lot. A plan may look affordable until you realize the out-of-network deductible is much higher.

To understand this better, read AHiX’s guide on how health insurance deductibles work.

3. Copays

A copay is a fixed amount you pay for a covered service.

For example:

- $30 for a primary care visit

- $60 for a specialist visit

- $15 for a generic prescription

- $75 for urgent care

PPO copays may be lower in network and higher out of network.

4. Coinsurance

Coinsurance is a percentage of the cost you pay after meeting your deductible.

For example, if your plan has 20% in-network coinsurance, you may pay 20% of the allowed cost while the plan pays the rest.

Out-of-network coinsurance can be much higher.

5. Out-of-Pocket Maximum

The out-of-pocket maximum is the most you pay in a plan year for covered services that count toward the limit.

For 2026 Marketplace plans, the out-of-pocket limit cannot be more than $10,600 for an individual and $21,200 for a family. This limit applies to covered essential health benefits, and plans can set lower limits.

Important: Monthly premiums usually do not count toward the out-of-pocket maximum. Out-of-network costs may also follow different rules depending on the plan.

PPO Plan vs Metal Tier: Do Not Confuse These Two

Many people confuse PPO with Bronze, Silver, Gold, and Platinum.

They are not the same thing.

A PPO is a network type. It tells you how you can access doctors and hospitals.

A metal tier is a cost-sharing category. It tells you how costs are generally split between you and the insurance company.

Marketplace plans are grouped into Bronze, Silver, Gold, and Platinum categories, and those categories are based on how you and the plan share costs, not the quality of care.

So you may see:

- Bronze PPO

- Silver PPO

- Gold PPO

- Platinum PPO

The PPO part explains provider access. The metal level explains cost-sharing.

For a deeper breakdown, read AHiX’s guide on Bronze vs Silver vs Gold Insurance.

What Does a PPO Plan Usually Cover?

If your PPO is an ACA-compliant Marketplace plan, it must cover the 10 essential health benefits.

HealthCare.gov says Marketplace plans cover essential health benefits such as doctors’ services, inpatient and outpatient hospital care, prescription drugs, pregnancy and childbirth, mental health services, and more. Marketplace plans must cover essential health benefits across all metal levels and plan types, including HMO and PPO plans.

These categories usually include:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Pregnancy, maternity, and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative and habilitative services

- Laboratory services

- Preventive and wellness services

- Pediatric services

However, plan details still vary. The exact doctors, hospitals, drug formulary, copays, deductibles, and prior authorization rules can be different from one PPO plan to another.

That is why you should never choose a PPO only because the plan name looks familiar. Always compare benefits, costs, and network details.

PPO Plan Pros and Cons

A PPO can be a strong option, but it is not automatically the best plan for everyone.

PPO Plan Pros

| PPO Advantage | Why It Helps |

| More provider choice | You may have access to a wider list of doctors and hospitals. |

| No referral for many specialists | You can often schedule specialist care directly. |

| Out-of-network flexibility | You may still get some coverage outside the network. |

| Good for frequent travelers | A broader network can help if you need care in different areas. |

| Good for ongoing specialist care | Helpful if you already see certain doctors. |

PPO Plan Cons

| PPO Drawback | Why It Matters |

| May cost more | Premiums or cost-sharing may be higher than those of stricter plans. |

| Out-of-network care can be expensive | Coverage does not mean low cost. |

| More details to compare | You must check network, deductibles, coinsurance, and drug coverage carefully. |

| Balance billing risk | Out-of-network providers may bill more than the plan allows in some cases. |

| Not always available | PPO options vary by state, county, and insurer. |

When Does a PPO Plan Make Sense?

A PPO plan may be a good fit if you want flexibility and are willing to compare costs carefully.

A PPO May Fit If You:

- Want to see specialists without referrals

- Already have doctors you want to keep

- Travel often or live in more than one area during the year

- Want out-of-network options

- Have a family with different doctor needs

- Need regular specialist care

- Prefer more control over provider choice

- Are comfortable paying more for flexibility

A PPO May Not Fit If You:

- Want the lowest monthly premium

- Rarely visit doctors

- Are comfortable using a smaller network

- Prefer a primary care doctor to coordinate everything

- Do not need out-of-network coverage

- Want a simpler plan structure

- Have a tight monthly budget

For some people, an HMO, EPO, ACA-qualified plan, short-term plan, or non-qualified option may make more sense depending on their needs. You can compare plan types through AHiX’s individual health insurance plans, family health insurance plans, qualified health plans, and non-qualified health plans.

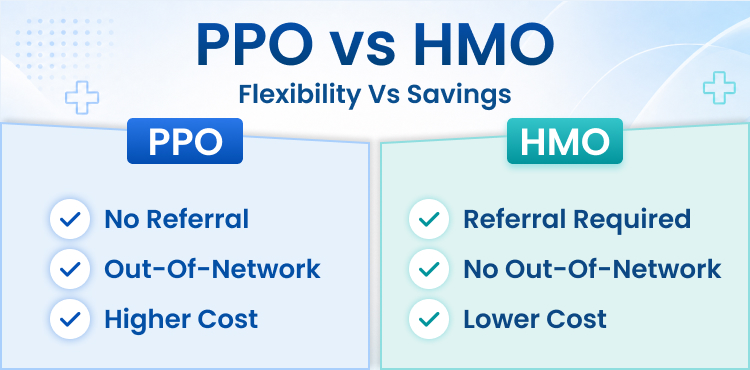

PPO vs HMO: Simple Difference

The simple difference is this:

A PPO usually gives you more freedom to choose doctors and specialists, including some out-of-network coverage, but it may cost more.

An HMO usually has a smaller network, may require a primary care doctor and referrals, and generally does not cover out-of-network care except in emergencies.

Here is a simple table:

| Feature | PPO | HMO |

| Provider flexibility | Higher | Lower |

| Specialist referrals | Usually not required | Often required |

| Out-of-network care | Usually covered at a higher cost | Usually not covered except in emergencies |

| Monthly premium | Often higher | Often lower |

| Best for | Flexibility and specialist access | Lower cost and coordinated care |

For a complete comparison, read HMO vs PPO Insurance in 2026.

PPO vs EPO: What Is the Difference?

An EPO, or Exclusive Provider Organization, may look similar to a PPO because it often does not require referrals. But the big difference is out-of-network care.

A PPO may cover some out-of-network care at a higher cost.

An EPO usually does not cover out-of-network care except in emergencies.

So, if you want no-referral specialist access but do not care about out-of-network coverage, an EPO may sometimes cost less than a PPO. But if you want the option to see providers outside the network, a PPO may be stronger.

PPO vs POS: What Is the Difference?

A POS plan, or Point of Service plan, combines features of HMO and PPO plans.

A POS plan may allow out-of-network care, but it may require you to choose a primary care doctor and get referrals for specialists. HealthCare.gov describes POS plans as plans where you pay less for in-network providers and generally need a referral from your primary care doctor to see a specialist.

A PPO usually offers more direct specialist access than a POS plan.

How to Choose the Right PPO Plan

Do not choose a PPO plan only because the word “PPO” sounds flexible. Two PPO plans can be very different.

Use this checklist before enrolling.

1. Check Your Doctors

Look up your current doctors, specialists, hospitals, and pharmacies.

Ask:

- Are they in network?

- Are they accepting new patients?

- Are they in the network for this exact plan name?

- Are they in the network at the location you use?

Do not rely only on a doctor’s office saying, “We take that insurance.” Ask whether they accept the exact plan.

2. Check Specialist Access

If you see specialists, check:

- Are your specialists in network?

- Is referral-free access included?

- Is prior authorization required?

- Are telehealth specialist visits covered?

- Are out-of-state specialists covered?

3. Compare Total Yearly Cost

Do not look only at the premium.

Compare:

- Monthly premium

- Deductible

- Specialist copay

- Prescription costs

- Coinsurance

- Out-of-pocket maximum

- Out-of-network deductible

- Out-of-network coinsurance

A lower premium PPO can still cost more if you use care often.

For cost planning, read AHiX’s guide on how much private health insurance costs.

4. Review Prescription Coverage

Check whether your medications are covered.

Look at:

- Drug tier

- Copay or coinsurance

- Preferred pharmacies

- Prior authorization rules

- Step therapy requirements

- Mail-order options

This is especially important if you take brand-name or specialty medications.

5. Review Emergency and Urgent Care Rules

Emergency care is treated differently from regular out-of-network care, but you should still understand the plan’s rules.

Check:

- Emergency room copay

- Urgent care copay

- Ambulance coverage

- Out-of-state emergency coverage

- Hospital admission rules

6. Compare PPO Against Other Plan Types

A PPO may be right for you, but it should not be your only option.

Compare it with:

- HMO plans

- EPO plans

- POS plans

- ACA-qualified plans

- Non-qualified plans

- Short-term plans, if appropriate for your situation

You can review available plan options through the AHiX health insurance plan grid.

Common PPO Mistakes to Avoid

Mistake 1: Assuming Every Doctor Is Covered

A PPO gives more flexibility, but it does not mean every doctor is affordable. Out-of-network care can be expensive.

Mistake 2: Ignoring the Out-of-Network Deductible

Some PPO plans have a separate deductible for out-of-network care. That means you may need to pay a large amount before the plan helps with out-of-network services.

Mistake 3: Looking Only at the Monthly Premium

A plan with a lower premium may have higher deductibles, higher specialist costs, or weaker drug coverage.

Mistake 4: Forgetting About Prior Authorization

Even if referrals are not required, approval may still be needed for certain services.

Mistake 5: Not Checking Prescriptions

A PPO network may look good, but if your prescriptions are expensive or not well-covered, the plan may not be the best fit.

Is a PPO Plan Good for Families?

A PPO can be a good option for families that want more provider choice.

This may be helpful if:

- Parents and children use different doctors

- A child sees a specialist

- Someone needs ongoing therapy or specialist care

- The family travels often

- You want access to a larger network

- You do not want referral delays

However, families should compare the family deductible and family out-of-pocket maximum carefully. For 2026 Marketplace plans, the family out-of-pocket limit cannot be more than $21,200, but many plans may set lower limits.

To compare options for your household, visit AHiX’s family health insurance plans page.

Is a PPO Plan Good for Individuals?

A PPO can also fit individuals who want flexibility and do not want a narrow network.

It may be useful if you:

- See specialists

- Travel for work

- Have an ongoing health condition

- Want to keep specific doctors

- Prefer direct access to care

- Are willing to pay more for choice

But if you are healthy, rarely use medical care, and mainly want a lower monthly premium, you should compare other plan types too.

AHiX’s individual health insurance plans page can help you compare options based on your needs.

Can You Get a PPO Plan Through the Marketplace?

PPO availability depends on your state, county, and the insurers offering plans in your area.

Marketplace plans can include different network types such as HMO, PPO, EPO, and POS, depending on what is available locally. HealthCare.gov notes that, depending on how many plans are offered in your area, you may find different plan types at different metal levels.

So, a PPO may be available in one county but not another.

If PPO availability is limited in your area, compare:

- HMO options

- EPO options

- POS options

- Qualified health plans

- Non-qualified health plans

- Short-term coverage, if suitable

For Marketplace-style coverage, start with AHiX’s qualified health plans page.

PPO Plan Checklist Before You Enroll

Before choosing a PPO plan, ask these questions:

- Are my current doctors in network?

- Are my preferred hospitals in the network?

- Are my prescriptions covered?

- What is the monthly premium?

- What is the deductible?

- Is there a separate out-of-network deductible?

- What is the specialist copay?

- What is the coinsurance after the deductible?

- What is the out-of-pocket maximum?

- Are referrals required?

- Is prior authorization required for common services?

- Does the plan cover out-of-state care?

- How much will I pay if I go out of network?

- Is the PPO available in my ZIP code?

- Does the plan fit my expected healthcare use?

If you are unsure, compare plans side by side before enrolling.

Final Thoughts: Is a PPO Plan Worth It?

A PPO plan can be worth it if you value flexibility, specialist access, and the option to use out-of-network providers. It may be especially helpful for people who already have preferred doctors, travel often, manage ongoing health needs, or want more control over where they receive care.

But a PPO is not automatically the best choice. You should compare the premiums, deductibles, copays, coinsurance, prescription coverage, provider network, and out-of-network rules before making a decision.

The best health insurance plan is not always the one with the most flexibility or the lowest premium. It is the plan that gives you the right balance of cost, access, and coverage for your real healthcare needs.

You can use AHiX Marketplace to compare health insurance plans, review individual coverage, explore family plans, and understand whether a PPO, HMO, EPO, qualified plan, or non-qualified plan may fit your situation.

FAQs About PPO Plans

1. What is a PPO plan in simple words?

A PPO plan is a health insurance plan that gives you more freedom to choose doctors and specialists. You usually pay less when you use in-network providers, but you may still have some coverage outside the network at a higher cost.

2. What does PPO stand for?

PPO stands for Preferred Provider Organization. It means the insurance plan has a preferred network of doctors, hospitals, and healthcare providers.

3. Do PPO plans require referrals?

Most PPO plans do not require referrals for specialists. However, some services may still need prior authorization before the plan will cover them.

4. Are PPO plans more expensive than HMO plans?

PPO plans often cost more than HMO plans because they usually offer more provider flexibility and out-of-network coverage. However, actual cost depends on the plan, insurer, state, county, metal level, and benefits.

5. Can I go out of network with a PPO plan?

Yes, many PPO plans allow out-of-network care, but you usually pay more. You may have a separate out-of-network deductible, higher coinsurance, or additional billing responsibility.

6. Is a PPO better than an HMO?

A PPO may be better if you want more provider choice, direct specialist access, and out-of-network options. An HMO may be better if you want lower costs and are comfortable using a more limited network.

7. Is a PPO plan good for families?

A PPO can be good for families that use different doctors, need specialist care, or want more flexibility. Families should compare premiums, deductibles, specialist costs, and out-of-pocket maximums before enrolling.

8. Can I get a PPO plan through the Marketplace?

PPO availability depends on your location and the insurers offering plans in your area. Some areas may have PPO options, while others may mainly offer HMO or EPO plans.