Most people assume health insurance is only available during Open Enrollment. But if something significant has changed in your life, losing a job, getting married, or having a baby, you may not have to wait. Qualifying events for health insurance can open a Special Enrollment Period, giving you a limited window to sign up for or change coverage outside the standard enrollment calendar.

Understanding what qualifies, how long you have to act, and what documentation you might need can make a real difference in staying covered. If you recently experienced a life change and are not sure where to start, AHiX Marketplace can help you compare available health plan options and connect you with licensed advisors.

What Is a Qualifying Event for Health Insurance?

A qualifying event for health insurance, sometimes called a qualifying life event, is a major change in your personal situation that may allow you to enroll in or change a health insurance plan outside the yearly Open Enrollment Period.

These events typically involve a significant change in one of four areas: your health coverage, your household, your place of residence, or your eligibility for government programs like Medicaid or CHIP. Not every life change qualifies, but certain events are recognized under federal and state rules as valid reasons to access health insurance outside the standard enrollment window.

Rules and eligibility can vary by state, plan type, and personal situation.

What Is a Special Enrollment Period?

A Special Enrollment Period (SEP) is the limited window of time during which you can enroll in health insurance because of a qualifying life event. Think of it as a temporary exception to the rule that you can only enroll during Open Enrollment.

Without a qualifying event, your options for getting covered mid-year may be very limited. But when you do have one, a Special Enrollment Period for health insurance gives you a set amount of time, often around 60 days, to find and apply for a plan. Missing this window may mean waiting until the next Open Enrollment season.

Common Qualifying Events for Health Insurance

Here are the most common situations that may trigger a Special Enrollment Period under federal Marketplace rules or state-based exchange programs.

1. Losing Employer or Job-Based Health Coverage

Losing employer-sponsored health insurance is one of the most common qualifying events. This can happen when you leave a job, whether you were laid off, quit, or your hours were reduced below the threshold that qualifies for coverage.

Example: If you were covered under your employer’s group plan and were laid off, you may be eligible to enroll in a Marketplace plan. This is also a moment when many people consider COBRA, which allows you to continue your previous employer’s plan for a period of time, but it is often more expensive than Marketplace alternatives. Comparing COBRA vs. Marketplace options after job loss can help you find better value.

2. Getting Married

Getting married is a qualifying life event for health insurance. If your new spouse has coverage through their employer, you may be able to join their plan. Or you may want to shop for a joint plan on the Marketplace.

Example: After your wedding, you have a window to add your spouse to your existing plan, switch to a family plan, or enroll in a new one together. Health insurance after getting married is something couples should address promptly rather than letting the deadline pass.

3. Having a Baby, Adoption, or Foster Care Placement

The birth of a child, the adoption of a child, or the placement of a foster child all count as qualifying events. These events allow you to add dependents to your current plan or enroll in a new plan that covers your expanded family.

Example: Once your baby is born, you typically have 60 days to add them to your coverage. Having a baby as a qualifying event for health insurance is critical to understand, because newborns are not automatically covered; you need to take action.

Note: Pregnancy alone generally does not trigger a federal Marketplace Special Enrollment Period. The birth of the baby is what counts. State rules may differ, so it is worth checking your specific state’s exchange if you are currently pregnant.

4. Moving to a New Coverage Area

Moving to a new zip code or county can qualify you for a Special Enrollment Period, but only if the move results in access to new health plan options that were not previously available to you. Simply moving to a new address within the same coverage area may not qualify.

Example: If you relocate from one state to another, you almost certainly will have access to different plans and insurers, making moving a qualifying event for health insurance in most cases.

5. Losing Medicaid or CHIP

If you lose eligibility for Medicaid or the Children’s Health Insurance Program (CHIP), you may qualify for a Special Enrollment Period to enroll in a Marketplace plan. Losing Medicaid as a qualifying event can have different timing rules than other events, so acting quickly is especially important.

In some cases, you may be able to enroll in Marketplace coverage before your Medicaid ends. Contact your state Medicaid office or check your state exchange promptly if you receive a notice that your coverage is ending.

6. Turning 26 and Losing a Parent’s Health Insurance

Under the Affordable Care Act, young adults can remain on a parent’s health insurance plan until they turn 26. Once they age off, this counts as a qualifying event. Turning 26 is a health insurance qualifying event that opens a Special Enrollment Period.

Example: If you turn 26 in April, you have a window to enroll in your own plan through your employer, a Marketplace plan, or another option. Do not wait until your birthday to start researching your choices.

7. Divorce or Legal Separation

Divorce or legal separation can be a qualifying event for health insurance if it causes you to lose coverage. For example, if you were covered under your spouse’s employer plan, and that coverage ends after a divorce, you may be eligible for a Special Enrollment Period.

Health insurance after divorce is an often-overlooked but important issue. Make sure you understand when your coverage ends under your former spouse’s plan so you can act before the deadline.

8. Death of a Covered Family Member or Policyholder

If the person who held your family’s health insurance plan passes away, the remaining family members may lose coverage. The death of a policyholder is a qualifying event that may allow surviving dependents to enroll in a new plan.

This is an understandably difficult situation, but it is important to address coverage quickly to avoid an insurance gap.

Events That May Not Count as Qualifying Life Events

Not every situation opens a Special Enrollment Period. The following circumstances generally do not qualify:

- Voluntarily canceling your current health insurance coverage

- Losing coverage because you did not pay your premiums

- Wanting to switch to a different plan because it is cheaper, without a separate qualifying event

- Moving to a new address within the same coverage area without gaining access to new plan options

- Missing Open Enrollment without a separate qualifying reason

If none of these apply, you may need to wait for the next Open Enrollment Period. However, it is always worth verifying that eligibility rules can be more nuanced than they appear.

How Long Do You Have to Enroll After a Qualifying Event?

In most cases, you have around 60 days from the date of your qualifying event to enroll in health insurance. This window applies to most federal Marketplace plans. Some state-based exchanges may have slightly different rules.

For certain events like losing Medicaid or CHIP, the timing may differ, and in some situations, you may be able to enroll before your current coverage ends. The key takeaway: do not wait. Missing the deadline could leave you uninsured and waiting months for the next Open Enrollment.

How long after a qualifying event you can get health insurance depends on the specific event and the plan type, so confirming your timeline early is a smart first move.

Documents You May Need to Prove a Qualifying Event

When you apply for a Special Enrollment Period, you may be required to submit documentation to verify your qualifying event. The type of document needed depends on your situation.

| Qualifying Event | Possible Documents You May Need |

| Loss of coverage | Employer letter, insurer notice, COBRA notice, Medicaid or CHIP termination notice |

| Marriage | Marriage certificate |

| Birth or adoption | Birth certificate, adoption papers, hospital record |

| Moving | Lease agreement, utility bill, mortgage statement, government mail |

| Divorce or legal separation | Divorce decree or legal separation document showing loss of coverage |

| Death of policyholder | Death certificate or insurance termination notice |

| Turning 26 | Notice showing removal from parents’ coverage |

Document requirements can vary by state, insurer, and plan type. Keep copies of any official letters, termination notices, or legal documents you receive related to your qualifying event. Having these ready before you apply can help avoid delays in your coverage start date.

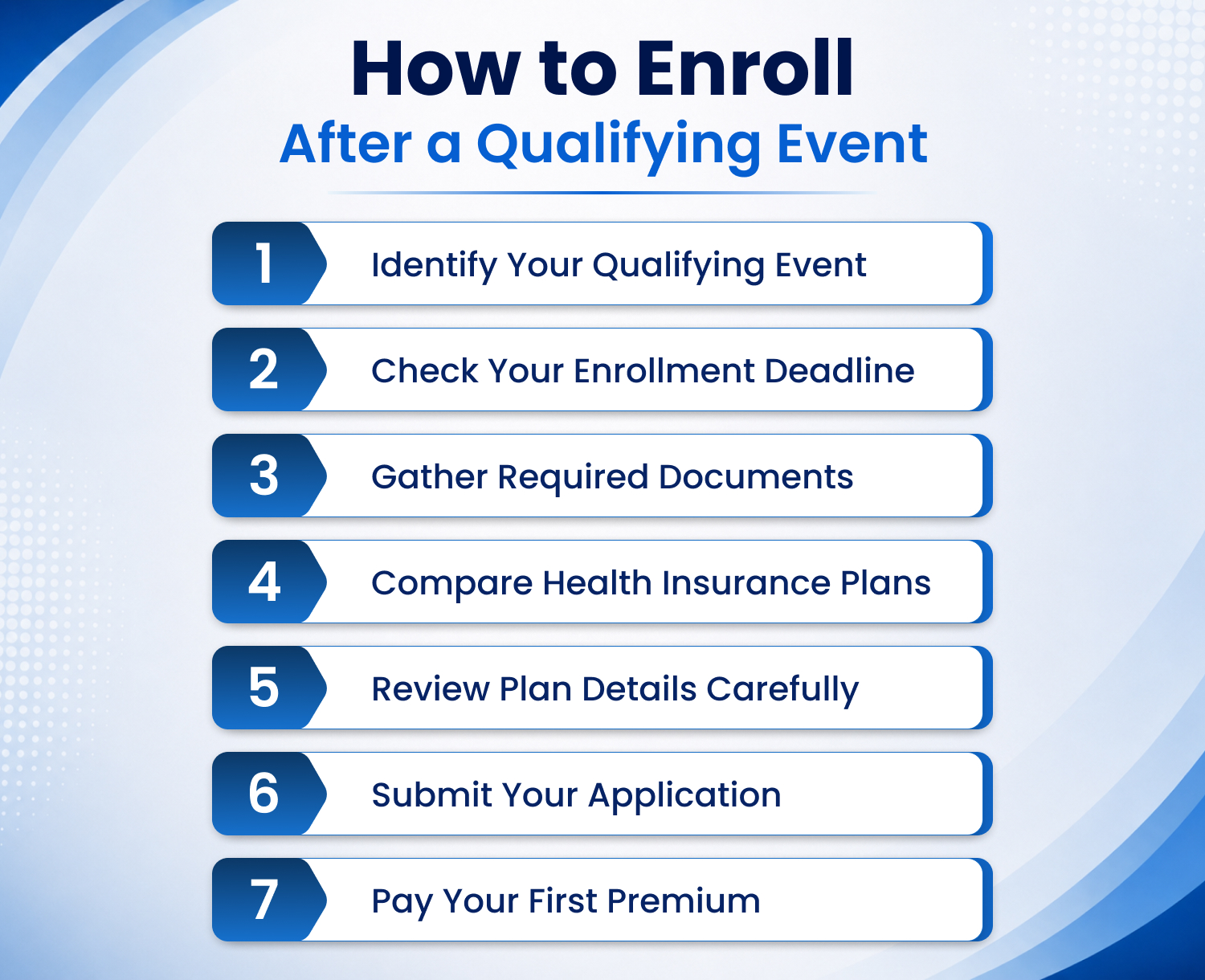

How to Enroll in Health Insurance After a Qualifying Event

Once you know you have a qualifying event, here are the general steps to get covered:

1. Identify your qualifying event:

Determine which life change you experienced and whether it is recognized as a qualifying event under federal or state rules.

2. Check your enrollment deadline:

Most events give you about 60 days, but confirm the specific window for your situation. Earlier is better.

3. Gather your documents:

Collect any paperwork that supports your qualifying event, such as a termination letter, marriage certificate, or birth certificate.

4. Compare health insurance plans:

This is where having a resource like AHiX Marketplace can be valuable. You can review individual, family, ACA, private, dental, vision, and supplemental plan options side by side, based on what is available and what fits your needs.

5. Review your plan details carefully:

Look beyond the monthly premium. Check the deductible, copays, prescription drug coverage, and whether your preferred doctors or hospitals are in the network.

6. Submit your application:

Complete the enrollment process through the Marketplace, your state exchange, or directly through a licensed advisor.

7. Pay your first premium:

Coverage does not begin until your application is approved and your first payment is made. Mark your payment due date so there is no lapse.

Qualifying Event vs. Open Enrollment

Open Enrollment is the annual period typically in the fall for coverage beginning January 1, when anyone can enroll in or change a Marketplace health plan, regardless of their circumstances.

A Special Enrollment Period, triggered by a qualifying life event, is different. It is a time-limited opportunity that applies only to those who have experienced a recognized life change. The coverage options may be similar, but the enrollment window is shorter and tied directly to your event date.

If you missed Open Enrollment and do not have a qualifying event, your options may be limited to short-term plans, Medicaid (if eligible), or CHIP (for children). Reviewing all available options quickly is important.

Can You Change Health Insurance Plans After a Qualifying Event?

Yes, in many cases, a qualifying event allows you to change your plan, not just enroll in one. Depending on the event, you may be able to:

- Add a newly born child or adopted child to your existing plan

- Add a spouse after marriage

- Switch to a different plan entirely after moving to a new state

- Transition from an employer plan to a Marketplace plan after job loss

Changing health insurance after a qualifying event is not just for people without coverage. It is also a chance to reassess whether your current plan still meets your needs.

How AHiX Marketplace Can Help

After a qualifying event, time is limited, and the decisions can feel overwhelming. AHiX Marketplace is designed to simplify the process. You can compare individual, family, ACA, private, short-term, dental, vision, and supplemental options all in one place, based on what is available in your area and what you qualify for.

Licensed advisors are available to help you understand your choices, explain the differences between plans, and walk you through the enrollment process. There are no exaggerated promises here, just real, practical support when you need it most.

Final Thoughts

Qualifying events for health insurance exist precisely to prevent people from falling through the cracks. A job loss, a move, a new baby, or a change in government coverage can disrupt your health insurance, but it can also open a window to get covered again quickly.

Act promptly. Confirm your eligibility. Gather your documents. And compare your plan options before your Special Enrollment Period closes.

Had a qualifying life event? Compare health insurance options with AHiX Marketplace and find coverage that fits your needs.

Frequently Asked Questions

1 What are qualifying events for health insurance?

Qualifying events for health insurance are specific life changes, such as losing coverage, getting married, or having a baby, that may allow you to enroll in or change a health plan outside the yearly Open Enrollment Period.

2 Is losing a job a qualifying event for health insurance?

Yes. Losing job-based health coverage, whether through layoff, termination, or reduced hours, is one of the most common qualifying events. It typically triggers a Special Enrollment Period of around 60 days.

3 Does quitting a job count as a qualifying life event?

It can. If you voluntarily leave a job and lose your employer-sponsored health insurance as a result, this is generally considered a health insurance qualifying event. The key factor is losing the coverage, not how the employment ended.

4 Is getting married a qualifying event for health insurance?

Yes. Marriage is a recognized qualifying event. After getting married, you and your spouse may have the opportunity to enroll together, add each other to existing plans, or shop for new coverage.

5 Does having a baby qualify you for health insurance enrollment?

Yes. The birth of a baby is a qualifying event that allows you to enroll in a new plan or add your child to an existing one. You typically have around 60 days from the birth date to take action.

6 Is moving a qualifying event for health insurance?

Moving can be a qualifying event if you relocate to an area where different health plan options are available. Moving within the same coverage area without gaining new plan options may not qualify.

7 Is pregnancy a qualifying life event for health insurance?

Under federal Marketplace rules, pregnancy alone does not typically trigger a Special Enrollment Period. The birth of the baby is what counts. Some states have different rules, so it is worth checking your state’s exchange if you are currently pregnant.

8 How long do I have to enroll after a qualifying event?

In most cases, you have around 60 days from the date of the qualifying event to enroll in a health plan. This window can vary depending on the event, state, and plan type, so it is best to act as soon as possible.

9 What documents do I need for a qualifying life event?

The required documents depend on your qualifying event. Common examples include a termination letter for job loss, a marriage certificate for marriage, a birth certificate for a new child, or proof of a new address for a move. Keeping copies of all official notices is recommended.

10 What if I missed Open Enrollment and do not have a qualifying event?

If you missed Open Enrollment and do not have a qualifying event, your options may be limited. Short-term health plans, Medicaid (if you are income-eligible), or CHIP (for children) may be available depending on your situation. Contact AHiX Marketplace to explore what options may still be accessible to you.