Being your own boss means you answer to no one, except, it turns out, the health insurance market. There’s no HR department picking a plan for you, no employer quietly covering 70% of the premium, and no payroll deduction making it all feel painless. If you’re a freelancer, gig worker, independent contractor, consultant, or sole proprietor, the bill lands entirely on you.

And in 2026, that bill looks different than it did a year ago. The enhanced subsidies that propped up Affordable Care Act premiums since 2021 expired at the end of 2025, and the old “subsidy cliff” is back. For a lot of self-employed people, especially the ones doing well enough to earn a comfortable living, that changes the math completely.

This guide walks through every realistic option you have, what each one actually costs, the tax break most 1099 workers forget to claim, and a simple framework for picking the right path. No jargon dumps, no fluff: just what you need to make a confident decision.

Short on time? Enter your ZIP code and compare plans in about two minutes, or call a licensed AHiX advisor at 800.800.5735 to talk it through with a real person.

Why 2026 Is a Pivotal Year for Self-Employed Coverage

Here’s the single most important thing to understand before you shop.

From 2021 through 2025, temporary federal enhancements made ACA marketplace plans dramatically more affordable and, critically, extended subsidies to people earning well above the old income limits. Those enhancements lapsed on January 1, 2026, reverting the rules to their pre-2021 form. The practical result is what analysts call the subsidy cliff: once your household income crosses 400% of the federal poverty level, premium tax credit eligibility doesn’t taper off. It vanishes entirely.

For 2026, that cliff sits at roughly $62,600 for a single person, $84,600 for a two-person household, and $128,600 for a family of four. Earn a dollar over the line and you can be responsible for the full, unsubsidized premium.

This matters enormously for the self-employed for one reason: your income is variable and often higher than you think. A good year, a big contract, a spouse’s bonus, any of it can push you over the cliff, sometimes after you’ve already enrolled. Marketplace premium payments rose by an average of about 58% heading into 2026, and the people who got hit hardest were precisely those above the subsidy line. They made up a small share of enrollees but nearly half of the people who dropped coverage.

The takeaway isn’t “the ACA is bad.” For many self-employed people, a subsidized marketplace plan is still the best choice. The takeaway is that 2026 is the year to actually compare your options instead of auto-renewing, because the alternatives now deserve a serious look. (Want the side-by-side? Our 2026 Health Plan Grid lays out how each category stacks up.)

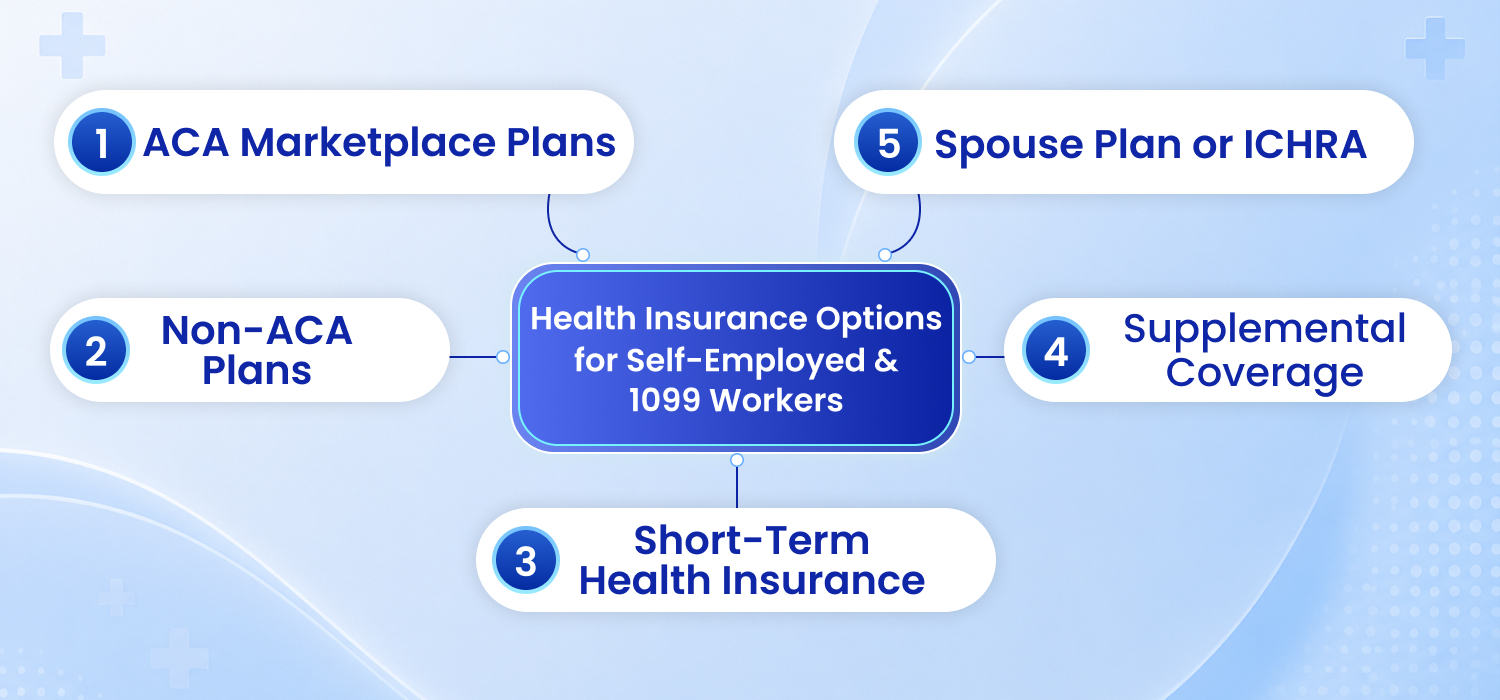

Your Realistic Options as a Self-Employed Person

You have more paths than most people realize. Here are the five that actually apply to 1099 earners, with the honest pros and cons of each.

1. ACA-Qualified Marketplace Plans (“Obamacare”)

These are the comprehensive, ACA-qualified health plans that cover all ten essential health benefits, accept you regardless of pre-existing conditions, and come in Bronze, Silver, Gold, and Platinum tiers.

Best for: Self-employed people who (a) have ongoing health conditions or take regular prescriptions, (b) want maternity, mental health, or substance-use coverage, or (c) still earn under the subsidy cliff and can get meaningful premium tax credits.

Watch out for: If you’re above 400% FPL in 2026, you pay full freight, and full-price ACA premiums for a 50-something couple can run well over $1,500 to $2,000 a month in some regions. Always estimate your income carefully, because guessing low and earning high can trigger a repayment at tax time.

2. Non-ACA / Non-Qualified Plans

Non-qualified plans don’t follow every ACA rule, which is exactly why they cost less. Many are built on broad national PPO networks (think Aetna or Cigna PPO access) and offer doctor visits, prescriptions, hospitalization, and surgical coverage, often with multi-year rate guarantees.

Best for: Healthy self-employed people who don’t see a doctor often, who are over the subsidy cliff, and who want real coverage for the big stuff without the full-price ACA premium. If you’re not sure how PPO access works, our explainer on what a PPO plan is and the HMO vs. PPO comparison are worth five minutes.

Watch out for: These generally don’t cover pre-existing conditions, maternity, mental health, or substance-use treatment. If you need any of those, an ACA plan is the safer choice.

3. Short-Term Health Insurance

Short-term health insurance is designed to bridge gaps: between leaving a W-2 job and your freelance income stabilizing, or while you wait for an ACA plan to kick in. It’s typically 50% to 80% cheaper than a comparable marketplace plan, and you can often be approved in a day.

An important 2026 note on duration: A 2024 federal rule capped short-term plans at roughly four months total. However, federal regulators stated in 2025 that they are not prioritizing enforcement of that limit while they reconsider the rule, so longer-duration plans have effectively returned in many markets. State law is the real deciding factor. About a dozen states ban or heavily restrict these plans, while others allow much longer terms. Check what’s available where you live on our plans-by-state page.

Best for: Genuinely healthy people who need a fast, affordable bridge and can pass basic medical underwriting.

Watch out for: Short-term plans are medically underwritten (you can be declined), exclude pre-existing conditions, and don’t cover preventive care or maternity. They’re a bridge, not a destination.

4. Supplemental Coverage (the piece almost everyone skips)

Whatever base plan you choose, supplemental plans such as accident, critical illness, and hospital indemnity, plus standalone dental and vision, pay cash benefits that help cover the deductible and out-of-pocket costs your primary plan leaves behind.

For the self-employed, this is the smart hedge. If you choose a lower-premium non-ACA or high-deductible plan to save money month to month, a first-dollar accident or critical-illness rider means one bad fall or diagnosis doesn’t wipe out your savings. Dental plans in particular start as low as $8.95/month, which is often less than a single out-of-pocket cleaning.

5. A Spouse’s Employer Plan, or Your Own ICHRA Once You Hire

Two easy-to-miss options:

- If your spouse has employer coverage, getting added to their plan is frequently the cheapest route, full stop. Run the numbers before anything else.

- Once your business grows and you bring on employees, an Individual Coverage HRA (ICHRA) lets you reimburse yourself and your team for individual coverage with tax-free dollars, often more flexible and affordable than a traditional group plan. It’s worth knowing this exists before you make your first hire.

What Self-Employed Health Insurance Actually Costs in 2026

Real numbers, with the honest caveat that your price depends on age, ZIP code, tobacco use, and plan tier.

| Option | Typical monthly cost (individual) | Covers pre-existing conditions? | Best fit |

| ACA-Qualified (subsidized) | $0 to $200+ if you qualify for credits | Yes | Lower income, ongoing health needs |

| ACA-Qualified (full price, over the cliff) | $500 to $2,000+ depending on age/region | Yes | Higher earners who need full benefits |

| Non-ACA / Non-Qualified | Often $300 to $500 | No | Healthy, over-the-cliff earners |

| Short-Term | ~$115 average | No | Short coverage gaps |

| Dental (standalone) | From $8.95 | N/A | Everyone: cheap peace of mind |

For a deeper breakdown of national averages and what drives them, see our guide on average monthly health insurance costs.

The headline for 2026: if subsidies don’t reach you, the gap between a full-price ACA plan and a non-ACA alternative can be several hundred dollars a month, which is exactly why comparing is no longer optional.

The Tax Break Most 1099 Workers Forget: The Self-Employed Health Insurance Deduction

Here’s money many self-employed people leave on the table every single year.

If you have a net profit from self-employment and you pay your own premiums, you can generally deduct what you spend on medical, dental, vision, and qualified long-term care insurance for yourself, your spouse, your dependents, and even your children under age 27. For the 2025 tax year and beyond, this is calculated on IRS Form 7206 and flows to Schedule 1 (Form 1040), line 17.

Why this is a big deal:

- It’s an “above-the-line” deduction, meaning you get it whether or not you itemize.

- It lowers your adjusted gross income, which can have ripple benefits across your whole return.

- It applies to dental and vision premiums too, not just major medical.

The important limits, so you don’t get tripped up:

- The deduction can’t exceed your net self-employment profit. If your business shows a loss, you can’t claim it that year.

- You can’t claim it for any month you were eligible for an employer-sponsored plan, including through your spouse’s job, even if you declined it.

- It does not reduce your self-employment tax, only your income tax.

This single deduction often changes the real, after-tax cost comparison between options. Always confirm the specifics with a tax professional, but don’t shop for coverage as if your premiums are non-deductible. For most 1099 workers, they aren’t.

How to Choose: A Simple Decision Framework

Run yourself through these questions in order.

- Does your spouse have an employer plan? If yes, price that first. It’s often the cheapest answer.

- Do you have pre-existing conditions, take regular prescriptions, or expect major care (including maternity)? If yes, lean toward an ACA-qualified plan. It’s the only category guaranteed to cover them.

- Will your 2026 income stay under the subsidy cliff? (~$62,600 single / ~$84,600 for two.) If yes, an ACA plan with premium tax credits is likely your best value. If you’ll be over it, keep going.

- Are you generally healthy and shopping over the cliff? Compare non-ACA / non-qualified plans. You may get solid PPO coverage for far less than a full-price marketplace plan.

- Do you just need to bridge a short gap? A short-term plan can cover you fast and cheap while you sort out the long-term answer.

- Whatever you pick, did you protect the gaps? Add supplemental or dental coverage so a surprise doesn’t become a financial emergency.

One more thing every self-employed person should know: you don’t have to wait for Open Enrollment if your life changes. Losing job-based coverage, getting married, having a baby, or moving can open a special enrollment period. For most states, the 2026 Open Enrollment window ran November 1, 2025 through January 15, 2026, but qualifying life events can let you enroll outside of it.

Frequently Asked Questions

1. Can I get health insurance if I’m self-employed with no employer?

Yes. Self-employed people buy individual and family coverage directly through the marketplace or through a licensed marketplace like AHiX. You have access to the same ACA-qualified plans as everyone else, plus non-ACA and short-term alternatives.

2. What’s the cheapest health insurance for a 1099 worker?

It depends on your health and income. If you qualify for premium tax credits, a subsidized ACA plan can be very cheap. If you earn too much for subsidies and you’re healthy, a non-ACA plan or a short-term plan is often the lowest-cost route. Standalone dental starts as low as $8.95/month.

3. Can I deduct my health insurance premiums if I’m self-employed?

Generally yes, if you have a net profit and aren’t eligible for an employer or spouse’s plan. The self-employed health insurance deduction is calculated on IRS Form 7206 and reduces your taxable income above the line. It can’t exceed your business profit. Confirm details with a tax professional.

4. What happens if my income goes over the subsidy cliff after I enroll?

This is the key 2026 risk. If your final income exceeds 400% of the federal poverty level, you can lose subsidy eligibility entirely and may have to repay advance credits at tax time. Self-employed people with variable income should estimate carefully and revisit their plan if a big year is shaping up. A non-ACA plan may end up cheaper than a full-price marketplace plan plus repayment.

5. Is short-term health insurance a good idea for freelancers?

It can be, as a bridge. It’s affordable and fast, but it’s medically underwritten, excludes pre-existing conditions, and skips preventive and maternity care. Use it to cover a gap, not as your permanent plan, and check your state’s rules first.

6. Does the type of plan affect which doctors I can see?

Yes. HMO plans keep costs down with a tighter network and referrals; PPO plans cost more but let you see specialists and out-of-network providers more freely. Many non-ACA plans are built on broad national PPO networks.

The Bottom Line

For the self-employed, 2026 rewards people who shop and punishes people who autopilot. With the subsidy cliff back, the right choice now depends more than ever on your income, your health, and your risk tolerance, and the gap between options can be hundreds of dollars a month.

You don’t have to figure it out alone. AHiX Marketplace lets you compare ACA, non-ACA, short-term, dental, and supplemental plans from leading national carriers in one place: free, with no obligation and no spam calls.

Compare self-employed health plans in about two minutes. Enter your ZIP code to see your options, or talk to a licensed AHiX advisor at 800.800.5735.

This article is for general educational purposes and isn’t tax, legal, or medical advice. Plan availability, benefits, and pricing vary by carrier and state. For full Qualified Health Plan information and official eligibility determinations, visit HealthCare.gov.